Make no mistake: for 95% of people in the world, investing in an ETF, specifically an ETF that tracks a major index like the S&P500, the TSX or any other important world index, is absolutely the way to go. To clarify even further, my advice to 90% of people with money to invest would be: “buy an index fund and forget all about it. You’ll earn 8-10% per year without doing any work at all and you’ll easily crush 90%+ of mutual funds on both returns and risk profiles.” One day, I will certainly make an entire post explaining why the average citizen should invest of his or her money in an index fund and nothing else and I will even explain the reason why and the way to do it.

With that in mind, here’s why I don’t like Exchange-Traded Funds

Contents

- 1 With that in mind, here’s why I don’t like Exchange-Traded Funds

- 1.1 And then a question pops in my head…

- 1.2 Why is XRE paying only a 4.63% dividend when most of its holdings pay over 5% dividend?

- 1.3 ETF: assume all the risk, only get part of the reward!

- 1.4 So not only does XRE steals your dividends, it grows more slowly too! What a farce!

- 1.5 Starting to get my drift?

- 1.6 What a joke!

- 1.7 When you buy ETFs, you help some rich asshole buy another private jet

- 1.8 But but but what about reinvesting!

- 2 Okay, but what about big index funds with low fees such as SPY?

- 3 Conclusion

Back in 2009, I was looking at getting some exposure to the Canadian real estate market. I thought it was a great sector: relatively safe (Canada was mostly unaffected by the 2008-2009 housing meltdown in the US), great dividend yields, no real recovery had happened yet, etc. I thought the sector would overperform in the coming years and I wanted to get some exposure to it.

As I didn’t know much about Real Estate at the time, and as I had a maximum of $10,000 to invest in that particular project, my normal reaction was to look at ETF, or exchange-traded funds. After all, a diversified financial instrument would certainly reduce the risk of holding separate securities, especially given how little money I had to invest. Furthermore, I would save massively on commissions by buying one and only one product, instead of several.

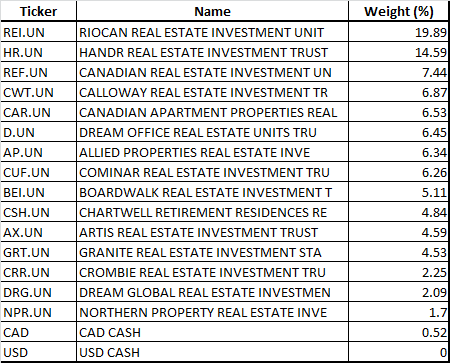

After doing some research, I found the top Real Estate ETF in Canada:

Now, Vanguard Real Estate is also pretty good, but I finally decided on TSE:XRE. One quick note: the “capped” simply means the fund will never have more than 25% of its money in a single security. Right now for instance, it even limits itself at 20% in one stock.

Anyway, so there I go, with my $10,000, I buy a thousand shares of XRE or so, I pay something like $10 in commissions (only!) and I’m all happy about it. “A good thing done!” I think. I hold the ETF until mid 2010 and, at this point, I basically obtained a 40% return and I’m ectasic about it. The fund decides to start paying a monthly dividend (wow! Who doesn’t like a free check every month?) and everything is going just perfectly.

And then a question pops in my head…

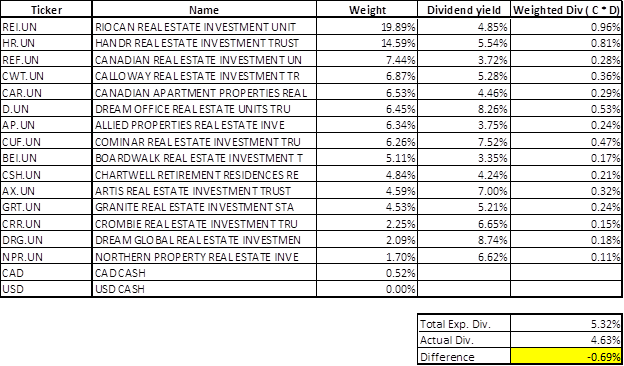

“Why am I receiving a 4.63% dividend when most of XRE’s holdings are paying 5% or more in dividends annually?”

It’s a good question, actually. Now, the rate at the time was the different, but the point remains: today, XRE pays a monthly dividend between $0.06 to $0.06936 (not sure why it varies so much when the distributions from REITs pretty much never change, but oh well), for a total dividend rate of 4.63% at the moment.

As some of you might know, XRE’s holdings are public. Public as in, you know exactly what is behind every share of XRE. Here they are:

XRE seeks to copy the Canadian Capped REIT index. This index reveals which 15 stocks it is composed of, but not in which quantities. In other words, you know that the Canadian Capped REIT index has money invested in CRR.UN, but not in what percentage. Trying to replicate an index is thus a delicate and sophisticated art, implicating tons of very good computers and advanced correlation studies.

Now, the question one million dollars question that should pop in your mind: why in the love of God wouldn’t you simply invest in the 15 securities yourself?

In other words, what prevents you from directly buying the securities listed ahead and saying “goodbye” to XRE altogether? Answer: nothing at all! And it’s not like this ETF is super-well diversified neither: four securities represent nearly 50% of its holdings!

As soon as I realized that, XRE was gone from my portfolio. I picked 10 REIT in that list, put $1,000 in each and voilà, done. I can tell you that the weakest investment in that list are NPR.UN, CRR.UN, GRT.UN, AP.UN and CAR.UN. These REITs aren’t “bad,” but they simply don’t compare to D.UN, BEI.UN or REF.UN.

Why is XRE paying only a 4.63% dividend when most of its holdings pay over 5% dividend?

Let’s say you replicated XRE’s portfolio; in other words, you devote a part of your portfolio to replicate exactly what XRE is doing. What would be the dividend you’d be getting then? Well:

The table above doesn’t lie. If you invested in securities yourself in the same weight as the ETF, you’d earn a 5.32% dividend per year, yet XRE only pays you 4.63%, for a difference of 0.69%.

In other words, holding XRE costs you 0.69% per year in lost dividends only! That’s… That’s not nothing at all! On my original $10,000 investment, that’s $69 I was throwing to the trash every year! Money that is simply WASTED and gone forever in the pockets of someone that is not me!

ETF: assume all the risk, only get part of the reward!

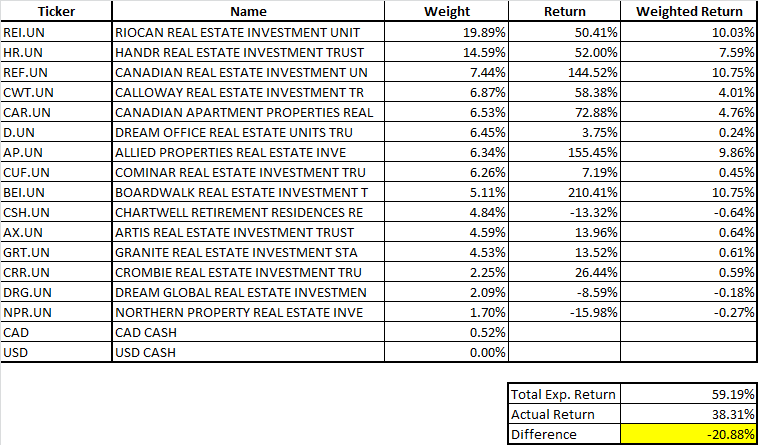

It’s not like the fund has offered a decent growth return over time neither. In fact, here’s the total growth rate in the last 10 years for every single of its constituents:

Returns, excluding dividends

Now, look at this: BEI.UN has returned over 210.41% return over the last 10 years (!) IN ADDITION to dividends! Overall, the portfolio as constituted would have returned 59.19% over the last ten years (plus dividends).

… and yet XRE returned only 38.31%!

So not only does XRE steals your dividends, it grows more slowly too! What a farce!

Now, it is true that an ETF rebalances as time goes. It’s also true that seeks to replicate an index and that it is kinda “stuck” doing whatever the index is doing. In other words, if the index decides to add GRT.UN as one of its component, XRE is “stuck” buying it. Still, the fact remains that no matter how you want to see it, XRE offers mediocre returns at best.

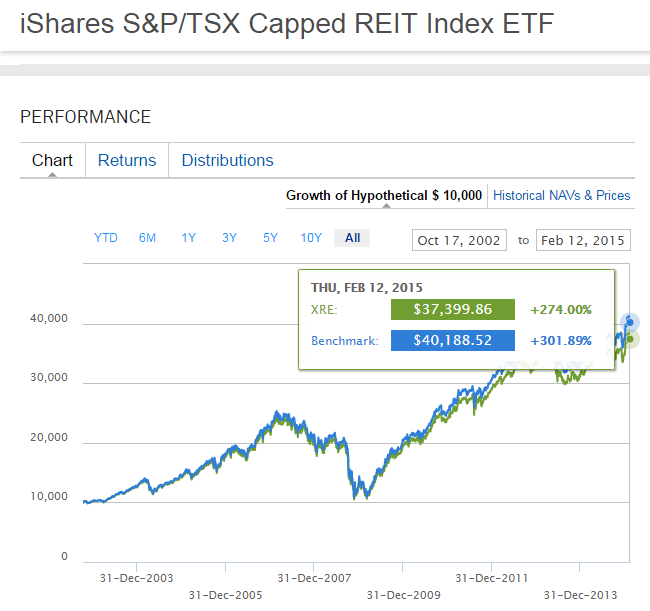

It even tells you itself. Look:

$2,888 gone thanks to this useless ETF: XRE

If you had invested $10,000 on the day XRE was created, you would have $37,399.86 today. However, if you had instead invested in the underlying assets directly, you would have $40,188.52 today! That’s a difference of $2,888! $2,888 of your money gone forever for no reason!

Starting to get my drift?

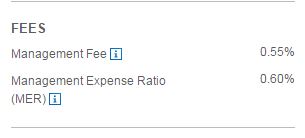

If you think about it, what iShares is doing here is pretty stupid: they just stand back and collect a 0.55% payment per year. Once every six full moon, it enters a few transactions to rebalance and adjust its positions. This is something even a middle school dropout could do, yet XRE and iShares charge ridiculous sums for it:

That’s right: XRE takes 0.55% of your money every year (that accounts for at least part of the missing dividends) IN ADDITION TO ALL TRANSACTION/MARKET/LEGAL FEES! And somewhat, somewhere, the fund also has to pay sales taxes! I’ve never heard of any sales taxes on any investment but somehow you, the pawn who holds shares of XRE, have to pay this.

What a joke!

At 0.55% per year and with a market cap of $1.3B, that’s $7,150,000 gone every year, and for what exactly? What does iShare do that is worth millions?

I mean, it’s not like what they do is hard. At least mutual funds (even worse than ETFs - more on that later) have to at least put up the appearance that they are trying to beat the market, but XRE? It copies an index! It only has to buy what the index has and rebalances from time to time! This is so stupid! I could do all of that easily for $100,000 a year, my salary and all fees included, and I would be working 2-3 hours per month at most!

When you buy ETFs, you help some rich asshole buy another private jet

Look: finance can be extremely complex. It goes extremely far and I won’t even begin to describe caplets, callonputs, conic optimization and whatever. The people who do that, honestly, earn their money. It’s hard and it requires a long education. Even most daytraders, in my opinion, earn their commissions and bonuses. But XRE isn’t tough finance: it’s just buying and selling shares according to a model that a dog could have developed in its sleep. I wonder how much the managers of that fund earn themselves. Chances are, this ETF is responsible for a few more millionaires in this country, and all of this for absolutely the most basic tasks of all times.

Now, I have to say that I don’t consider ETFs managers to be crooks: they tell you very clearly that you are getting ripped off and the fault lies on naive investors too lazy to peruse the prospectus. I mean, it’s not like they hide that fact: it’s plain as the light of the day. Still, at the end, millions are wasted year after year, millions that should be in investors’ pockets.

I don’t like ETFs and I never will, period

But but but what about reinvesting!

One advantage that is frequently touted by fans of ETFs is that you can easily add and remove to your position at any time without unbalancing your positions. For instance, if I had 1,000 shares of XRE and needed some money for some urgent project, I could just sell 100 shares and be done with it - no need for “complex” (cough cough) calculations to know what to sell and how much of it to sell.

Similarly, if I get a $1,000 bonus at work, I can just dumbit all into XRE (or any other ETF I choose) and not have to do any more work. Had I invested manually in the 15 stocks in the ETF instead, I would face the daunting tasks of manually investing my $1,000, choosing which stock to rebuy and how much of it.

In all cases, I could be facing tremendous commissions which would largely eat into my profits. For instance, at the $9.95 per trade most investors pay, investing in 15 companies would cost me $150. Given all that, a $69 price tag per year (taken from a lower dividend - this is in addition to lower growth which is harder to predict. The real cost is something like $200-220 per year), it would seem so, doesn’t seem that all expensive.

Needless to say, this argument is completely silly. Here’s why:

A) Lower and lower commissions

It goes without saying that it costs less and less money to trade. Not too long ago, to trade, you needed to call a broker directly, who then proceeded to do the trade for you. You can still do that, if you’re really, really stupid, but most people do it over the internet.

Even more recently, barely 10 years ago, it was rare to find a broker offering a commission under $30. Often, it went up to the hundreds for something as simple as buying shares. Today, I pay $1 per trade. That’s right: $1 per trade. Let’s say I wanted to invest my shiny new $1,000 into three different REITs: I would pay $3 in commission total. The same goes if you want to sell, really: gone are the days of crazy commissions that devoured your profits.

Truly, the internet killed - or should have killed - ETFs. Lower commissions render ETFs mostly irrelevant and superannuated. Really, buy the underlying stocks and stop wasting your time and money on ETFs.

B) DRIPs and automatic rebuying

DRIPs, or “Dividend reinvesting plans,” allow you to directly reinvest dividends into stocks. In short, instead of getting paid $100 per month in dividends, you are being given the equivalent in shares of the company. For instance, say FSCO is paying a $1 dividend per share and you have 1000 shares trading at $10 each. Instead of taking the $1,000 cash, you would receive 100 shares (100 shares x $10 per share = $1,000, same as the cash dividend). No commissions at all!

But it gets even better. Many dividend-paying companies offer a rebate on DRIP, meaning you would be getting your shares at a reduced price. Say FSCO gives you a 5% rebate if you choose to get shares instead of cash; instead of giving you 100 shares at $10 (for a total of $1,000), you get 105 shares (105 x ($10*0.95)=$997.5, the firm pays you the other $2.5 in cash). Yes, with that option, you even get 5 all-new, free shares!

Many brokers today offer you that kind of plan for absolutely free. You will not pay a cent in commission for it. Every month, you get more and more shares added to your portfolio instead of cash. Fantastic, isn’t it?

Okay, but what about big index funds with low fees such as SPY?

Those are the best investment for those who either a) know nothing about investing b) don’t care about investing at all c) don’t want to have anything at all to do with the stock market. It certainly beats holding your money in a bank account. SPY, for instance, charges a niggardly 0.10% per year, far below the 0.60% of XRE.

Still, I don’t like ETF, even index funds, for the following reasons:

1) It’s still a 0.10% fee, and it’s 0.10% too much

Not a ton, arguably, but this is still money wasted, and I hate wasted money. Take a $100,000 portfolio - that’s $100 gone every year for pretty much little reason. Why pay for something you could get for free?

You know, the other day, I was at Costco and I noticed a water dispensary system on sale. Basically, you put one of those stupid blue plastic bottles that you have to pay for in it and you have water. I considered buying it, before I remembered water was actually free. Why would I do that, why would I waste money? There might be a day I become scared of fluor in water and actually start spending real dollar on some purifier thingy, but that day is not today.

2) You lose a lot of control

With an ETF, you truly are at the mercy of the managers of the index fund. Now, for SPY, the risk is minimal, but for many ETFs, you often simply don’t know what these guys are doing behind closed doors. For instance, what if they choose to rebalance and it creates a massive capital gain for the year? What if they choose to reduce their monthly dividend because… because they decided so? You are truly at the mercy of the managers of the ETF and their every move dictates how your portfolio will go.

What if the ETF decides to increase its fees, for example? For instance, right now, SPY offers a fee rebate of 0.0153% until Feb 1st, 2016. What will happen when the rebate ends? And what if the management fee ends up increasing even more? What about buyouts? For instance, what would happen if Blackrock, the managers of XRE, are bought out by another company, and the other company decides to change things around?

Oh, want to get rid of a dying stock? Well, you can’t - you can only sell the entire index! Truly, you lose a lot of control by buying an ETF.

3) Adds up more possibilities for fraud

It’s never good to add an intermediary in the first place, especially when needed. Now, to my knowledge, there has never been any ETF scandal in the history of finance, and the companies managing those ETF are well-insured and protected but…

… remember the financial crisis? I’m more or less curious what happened to the funds managed by Bear Sterns, Lehman Brothers and the hundreds and hundreds of bank who failed during that crash.

That’s not even counting the possibilities of outright fraud. Sure, ETFs are closely monitored and have to adhere to strict accounting standards, but… Well, you do remember Bernard Madoff, right? For decades, he was able to maintain his scam right under the nose of regulators. Am I right to be slightly worried about the possibilities of some funds managers being potential fraudsters? Sure, the risk that an ETF will be revealed to be a scam are microscopic at best, especially for a fund as large as the SPY, but why take the risk when you don’t need to?

4) You get a tiny, tiny part of your money invested in actually “great stock”

Let’s face: there aren’t that many “great” companies looking forward. In fact, SPY is filled to the brim with dinosaurs and companies I would rather never invest into. Look guys: I love Wal-Mart just as much as the next guy, but it’s simply too late to invest in it. The money has been made, game over, move on to the next stock.

Looking at what constitutes the SPY (page 33-37), I can think of perhaps 20-30 companies I would really want to invest into. So… why wouldn’t I invest into them directly instead? Truth be told, there are a lot of fillers in the SPY - companies that are there for the sake of being there because they create a nice, balanced S&P 500 index that covers all sectors and domains “fairly.” Take Hewlett-Packard for instance, the biggest piece of shit the stock market has ever produced. Who would seriously want to have money invested into that garbage? NYSE:HPQ is the company I think about when someone mentions “terrible company that has never done anything right, ever.” When was the last time HP produced anything relevant? Thought so. HP is the only large company company I can think of that somehow managed to hit a new low years after the financial crisis ended and every single of its products is utterly terrible and broken.

Again, as soon as a business hits a certain capitalization, the S&P500 kinda “has” to include it. But it doesn’t mean it’s a business I’d like to invest into. All those fillers reduce the percentage of your money is really invested into really great companies that compose the index,. Great companies like Abbvie, Apple, Gilead, Google, Haliburton, Intel, Kraft, Qualcomm, United Technologies and so on.

With so many bad companies in your ETF, you have a smaller piece of the really tasty stocks.

5) … and you are stuck with a lot of crap

Again, take a look at SPY’s numerous holdings, for instance. Who would want to have money invested in Yahoo? I would rather buy T-Bonds with negative interest rates than invest into this dying piece of garbage. Seriously guys: if I had to give you the choice between investing in Apple, Google, Microsoft, IBM, Akamai, SanDisk, Verisign or fucking Yahoo, what would you choose last? I mean, Yahoo, seriously? Why would anyone want to put money there when they could put it in Apple - hell, even Amazon is a better choice! Seriously, who would want to put their hard-earned money in Yahoo? Why not Blackberry while we’re at it? Because “it’s so low it has to go back up,” right?

If that’s not enough for you, how about “ticking bomb” Gamestop, “I am the next RadioShack” Best Buy, “I have no idea how we are still even in business” Staples and tons of other useless businesses that have absolutely no future? Why not “the fad has passsed” Groupon, “we can’t do anything right” Zynga and “one-trick-pony” King while we’re at it?

Call me hardcore, call me intransigeant, call me an aficionado, but I like to know exactly what I’m investing into. Looking at what constitutes SPY, I have no idea what half of these businesses are. Can you tell me what Mohawk Industries is? How about Nucor Corp, Snap-on Inc. or Torchmark Co.? Chances are, unless you worked for those companies yourself, you have as little clue as me as to what they are, and if you don’t know what they are, why in the love of yolo would you want to invest in them?

6) Finally, not many people remember the great lesson of Nortel

At one point, Nortel represented 33% of Canada’s main stock market. Its top valuation was insane at $440 BILLIONS and that was more than a decade ago. All this to say, if you were invested in a Canadian index ETF at the time, what do you think happened? Yep.

Do you think it makes sense to have 33% of your portfolio, ETF or not ETF, into one company? Hint: it does not. This fiasco actually was one of the reason leading to “caps” on indexes, but the fact remains that even ETF run the risk of being overexposed to an asset.

Buying a stock just for the sake of buying a stock, just because “everyone is doing it,” is not a good reason to buy a stock. It is true that, today, funds are more diversified. But looking at XRE - nearly 50% of its holdings are in three stocks. If only one of those ended up crashing, you would have a serious loss for the year.

No, really: pick 20 stocks in different sectors. Pick great stocks in great sectors that you feel confident are going to be around in ten years, with decent growth opportunities ahead. I’m talking of companies like Apple, GE, Pfizer, Disney, Caterpillar, Costco, McDonald’s, Kraft, etc. Put 5% of your money into each; many brokers offer 50 trades for free when you open an account, so do that, and reinvest the dividends when applicable. Then look away from the computer for 5-10 years. Or better yet, reinvest every month so you can average down when the market falls. Chances are overwhelmingly in your favor that you will absolutely crush the SPY.

Conclusion

ETFs definitely have a role to play in the financial world, but they simply aren’t for me and I would never invest into them. Make no mistakes: they are 10,000 times better than mutual funds, but they’re still ripe with problems and I see no reason to not simply buy the stocks directly.

I don’t get it. The stock market is possibly the eighth wonder of the modern world. Why would anyone buy ETFs when they can buy stocks instead? Unless you have a tiny amount of money to invest - like, under $5,000 - you are far better off buying stocks and saving whatever scam fee ETFs charge, in addition to having complete control on your finance.

I’d still recommend ETFs to people who really, really don’t want to spend a second thinking about finance (some people get sick just thinking about what a share is much like I get sick when I think about open heart surgery), but only major ETFs with extremely low fees. Even there, you can be sure none of my friends or family members have a penny in any ETFs.

Great article.

I took a bit of a long road to come to this same conclusion.

Originally I was with Financial Advisors and investing in those high priced Mutual funds, that give them a nice commission, and are designed to under perform the market.

Then I broke out of that and moved to low fee Index ETF’s.

A vast improvement yes, but why leave even a little money on the table?

Now I still have some cash in ETF’s but I’ve been opportunistically switching this out to high quality, dividend paying stock.

I definitely have my share of bruises but at least those were self inflicted and not at the whim of some genius fund manager.