My most recent transaction, aptly named “YOLO,” has garnered quite a bit of attention, and I have received some excellent questions. I think it is worth exploring some of them here. First, here is the transaction in question:

100 lots of 100 shares, at a premium of $3.17 (plus commission). A $31,800 gamble, basically. Market value at the time of taking this picture: $31,200.

Yes. I bought $31,800 of calls on Apple. Not stocks - call. Options. Derivative products.

First, I want to say that entering this position was a carefully planned, designed, considered and evaluated decision. It wasn’t done on a whim nor is it a spur-of-the-moment trade. I would NEVER have invested such a large of money was I not utterly convinced the bet I was about to take had an outstanding risk/reward profile.

Believe it or not, I consider myself a risk-averse investor in general. For instance, I didn’t play Netflix’s latest earnings and I didn’t short GoPro despite clear signs to this effect, simply because I considered both trade plays dangerous and too risky for me. While those two trading positions were in my opinion quite likely to be quite profitable, the risk that was associated with them was too much for me given the potential payouts and associated probabilities.

All this to say, for my massive call position on Apple, I have spent well over 50 hours planning the trade and studying how it would go down, what could possibly happen and how I would react shall certain scenarios materials. In clearer terms, I have spent the major part of last week studying every single element of data I could get my hands onto and I have spent the entire week-end in front of my computer to really evaluate whether this would be a good trade or not.

In this post, I will explain my full, complete and exhaustive thought process behind behind this massive gamble, and the reasons why I did what I actually did. I will detail every decision and why I believe my decision to buy 100 lots of 100 February 20, 2015 calls on Apple regular shares at a strike price of $110 was the right one.

Without further ado, here are some questions I received. The table of content that follows presents the various question I received, although the whole is meant to be read in order.

Contents

- 1 What did you buy exactly?

- 2 Okay, but why did you do that?

- 3 Why do you believe Apple to be “critically undervalued?”

- 4 “F.S.Comeau, I am still unconvinced!”

- 5 But F.S, The market has already anticipated that!

- 6 Okay, but the market has still anticipated strong earnings!

- 7 Okay, but even if Apple posts a beat, the stock might not rise…

- 8 I suppose this is where you keep your “ace in the hole”

- 9 One last thing

- 10 So, it’s all roses and daisies and ponies?

- 11 The potential problems

- 12 Do you plan to sell your options pre-earnings?

- 13 Why a February 20th, 2015 call? Why not a January 30th call if you want to play the earnings?

- 14 Why not hedge your position! You are way overexposed! Sell some $115 calls

- 15 Why not sell puts instead?

- 16 How are you feeling right now?

- 17 This sounds so cool! Should I do the same thing as you and buy Apple calls?

- 18 Final words?

- 19 No question, just wanted to say you are insane, but good luck!

What did you buy exactly?

I bought calls, which are options - but not the obligation - to buy Apple, at or before the market closes on February 20, 2015, at a price of $110. To do that, I had to pay a premium of $31,800 USD exactly. Yes.

If Apple is worth $140 at that date, each one of my call is going to be worth $30 because I can buy Apple as $110 and immediately resell it at $140, earning $30 (times 100 lots, times 100 shares - yeah, you get the picture). If Apple is worth $109.99 at that day, I lose my $31,800 because my options are worthless: I will not buy a stock for $110 using my options when I can buy it for cheaper on the open market (at $109.99).

In other words, there is a significant chance for me to lose 100% of my original investment, that is, $31,800, in that trade. More on that later.

Okay, but why did you do that?

Because it is my inner belief that a) Apple is critically undervalued at the moment AND b) is about to go far higher after earnings, which will be released Jan 27th, 2015. Had either of those elements not existed, I wouldn’t even have considered this strategy.

Given those beliefs, I sought to profit from what I believe was a market mispricing by buying call options on the stock. If I am proved right, and quite honestly I hope I am proved right, then this position should be massively profitable for me in the short term, albeit not at a low risk.

Why do you believe Apple to be “critically undervalued?”

Because when you look at the situation from a standard, unbiased and logical point of view, Apple’s valuation makes no sense. It is far, far, far, far, FAR lower than it should be. Icahn recently went on record saying Apple should be trading near $200 and while I do not agree with such a high price (which was mostly him talking to boost up the price of Apple), I agree with his overall sentiment.

Currently, Apple is trading at a ratio of 16.91. Let’s remove the cash on hand ($180B), less 30% for foreign taxes (a large part of which is already accounted for but let’s ignore that for now), and let’s remove Apple’s minuscule debt: we now have a P/E ratio of 13.6. That’s right: Apple is currently trading at a ratio LOWER THAN JNJ, KRAFT, COCA-COLA OR MCDONALDS!

But F.S., Apple is not Coca-Cola or Kraft or Johnson & Johnson or McDonald’s!

You’re right - Apple is far superior to those.

While those four examples are barely growing, and sometimes actually declining, Apple is still on fire and still growing in the double digits. And don’t even get me started about comparing it to GOOG or MSFT, all of which Apple has a much lower P/E despite being, well, you know, “meh” companies in general. To be clear, my point isn’t that Microsoft or Google are bad companies, they are just far less good than Apple (at this price)

All this to say, had Apple not been critically undervalued when compared to its peers, I wouldn’t even have considered any such kind of trade on Apple.

But wait! There is more!

As recently as a month ago, Apple was trading at $119, which puts its post-cash P/E at a more reasonable (but still too low given its growth) 16. When I entered my position, it was hovering over $106. There was absolutely no reason whatsoeverfor that 10% drop and if you think this is “normal,” we are talking of $60B market value vanishing in a month. SIXTY BILLIONS! Just due to normal daily volatility, Apple lost in **TWELVE BLACKBERRY** in market value! This is insane and no matter how hard I tried to justify this fall, I couldn’t do it. Trust me: I tried to understand why Apple dropped 10% while the overall market dropped a much lower 3% and I simply couldn’t find a reason.

All this to say, the table was set for exactly what I wanted to do.

Now, the main reason I entered this trade: the earnings

It is rather clear that, with my options expiring a little under a month from now, that I am playing a massive gambit on Apple’s earnings, which are due Jan 27th, 2015. If the earnings are awful for some reason, or even if the earnings are decent but disappoint the street, the stock will most likely crash and I will lose almost all of my investment, if not the entirety of it. Yes, I could very well lose 100% of my money in that trade because a $110 call expiring a month from now is not going to be worth much if Apple falls to $90, simply because the likelihood of Apple going up $20 within three weeks is minimal at best, especially with few catalysts in sight. In fact, with a remaining duration of 3 weeks until expiration, that option is worth around $0.25 according to the Black-Scholes model, very far from the $3.12 I paid for the stock.

All this to say, if the earnings are not absolutely phantasmagoric, I am toasted.

A good thing they will be, then!

Apple’s earnings are going to be stellar. Think, more stellar than stellar. Think, Samsung is going to have to change the name of its product line because Apple is going to be bigger than a galaxy. Here’s why.

For the first time ever, Apple had its flagship products (that is, the iPhone) for sale in EVERY SINGLE IMPORTANT COUNTRY IN THE WORLD. In fact, Apple’s sales are mostly in USA, Japan, China, Europe, India, Latin America, in that order. And guess what? Sales exploded in EVERY SINGLE OF THESE COUNTRIES. The most recent report of mobile phone usages show Apple significantly gaining on not one phone, not two, but EVERY SINGLE ANDROID PHONE IN THE WORLD! Oh, Android is still dominant, but Apple is without one doubt stealing customers from them.

12.2% gain in UK? Holy ****!

If you’re not convinced, think about it that way: iOS has, let’s face it, one phone. Sure, there are multiple version of it, but if you ask people what phone they are going to buy, here are what they will tell you:

iPhone, Galaxy, Note, HTC, Xperia, Microsoft Phone, Nexus, Droid, Moto G, OnePlus, LG, Lumia, Ascend, Optimus, Blackberry..

See where I’m going at? ONLY ONE PHONE IN THIS LIST IS IOS! Sure, there are different models of iPhones, much like there are 10,000s of models of Galaxy, but the fact remains that when somebody wants an iPhone (which I do), he wants an iPhone, and the model he ends up buying is irrelevant, because he’s buying an iPhone! Overall, analysts are comparing ONE product to EVERY SINGLE PHONE THAT USES ANDROID, and there are THOUSANDS of those!

Of all the phone in existence, only one has iOS, and Apple is somehow managing to crush every single Android phone in the world. Oh, and in the list above, I didn’t even include less-than-smart phones.

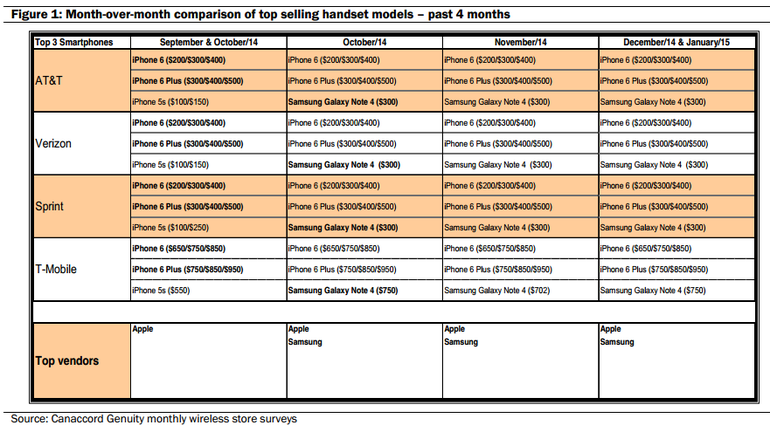

A fairer comparison would be to compare iPhone sales to Galaxy, HTC or Xperia sales. Let’s look at that right now:

Now, look at the table above. Look at it closely.

THE iPHONE5s OUTSOLD THE GALAXY NOTE 4 IN THE BIGGEST US CARRIER IN THE VERY MONTH IT WAS RELEASED

Forget the iPhone6 and iPhone6+. PEOPLE IN OCTOBER 2014 WERE MORE INTERESTED IN BUYING a 2013 phone that a phone released THAT VERY MONTH. I know I’m repeating myself, but it’s worth repeating. Now, take back the iPhone6 and iPhone6+.

Do you start to understand me a little?

Okay, but why?

Because iPhone6 and iPhone6+, that’s why. Now, I don’t want to blast Android, but name me ONE reason why people would buy an Android over an iPhone. What are people going to tell you?

“The bigger screen.”

But guess what? APPLE JUST RELEASED NOT ONE, BUT TWO PHONES WITH AWESOME BIG SCREENS! And to make matters even better, have you ever seen them? They are BY FAR the best phones I have ever seen, and I don’t speak just because I like Apple a lot. Just go see an iPhone6 or an iPhone6+ and tell me those aren’t the best phones on the market. Awesome camera, awesome screen, iTouch, awesome customer support, superior ecosystem, more stability, more responsive, uniform experience, Apple Pay (lol! More on that later), ease-of-use, lightweight, outstanding resolution, outstanding applications, outstanding quality, the list of perks is long and, no matter what people will say, the iPhone is still the best phone on the market.

Given all that, tell me what would you bet on:

- Earnings being meh

- Earnings being okay

- Earnings being outstandingly oustanding

- Earnings being so good you are going to have a heart attack and reincarnate as an iPhone

Still not convinced? Last holidays season (2013), Apple sold 51M and the year before that, 47M. Keep in mind that, at that time, the iPhone was not available in several key markets, and keep in mind the 5S had MASSIVE supply problems, and keep in mind this was the “S” cycle and not the all-cool, shinier, cooler, thinner 6. Now, consider that the P and 6+ had a one-month backlog for most of the last quarter DESPITE much higher supply, keep in mind the first week-end sales OBLITERATED last year’s sales (10M vs 6M despite a buggy website and strained supply) and keep in mind the iPhone was launched in pretty much every important country in the world by the end of October, giving two months of awesomeness and sales.

Still not convinced? Add-in the 5S and 5C which STILL ARE BEST-SELLERS TODAY, and even add-in the 4S which is still for sale in some key markets. Add in that the economy has improved a lot since 2013, add in lower gas during the period and thus more discretionary spending, add in the fact the mobile phone market is growing in the double digits in general, add in the fact the iPhone is, well, the iPhone, and what do you get?

“F.S.Comeau, I am still unconvinced!”

Okay then… Let’s consider last quarter’s sales (2014Q3). Total iPhone sales were 39.27M, far above 2013Q3’s 33.8M. Now, add-in the fact Apple crushed estimates with $8.5B in profits (when compared to $7.5B a year before that). “Hmm, a 13% rise in profits year-over-year for a company valued at $600B! Not bad!”

Now, how long were the all new and incredible iPhone6 and 6+ for sale last quarter to give such an outstanding result?

12 DAYS!!!!!!

Now, calculate the sales increase over not 12 days, but a full quarter - 92 - and what do we get?

Yeah.

Now, let ask you again: how many iPhones do you think Apple sold?

Answer: A TON.

More than a ton, THOUSANDS OF TONS.

Last holidays, Apple sold 51.03 millions. This year, my money is on, over 70M. Given everything I just said, do you start to understand why I made that trade?

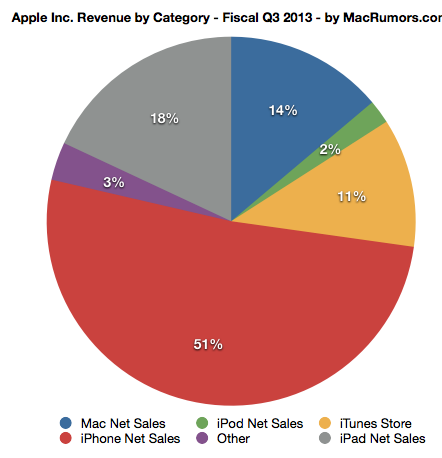

Have I spoken about iPads, Macs and iTunes revenues?

http://cdn.macrumors.com/article-new/2013/07/apple.png

Would it really surprise you that iTunes just reported pretty much a record number of sales and that Macs are rumored to also be excellent sellers?

WHAT ELSE DO YOU WANT?

Seriously, tell me. What else do I need to tell you to prove that Apple is going higher following stellar earnings?

At this time, only the iPad worries me slightly, and only because it probably won’t post much of a raise year over year. Is that honestly such a big deal? Is that going to spoil the entire earnings report? Well, I spent a lot of time last week studying the question, and my belief is that it won’t. I believe iPad sales are going to show a tiny rise from last year, but in my mind, this is going to be far from enough to prevent the stock from soaring post-earnings.

But F.S, The market has already anticipated that!

No, it has not. It absolutely has not. Apple is perhaps the most misunderstood stock in the history of the stock market and almost every single analyst who follows Apple misses the point of the company entirely. Don’t believe me?

http://aaplinvestors.net/stats/ipod/killerwatch/

http://aaplinvestors.net/stats/iphone/iphonedeathwatch/

http://aaplinvestors.net/stats/ipad/ipaddeathwatch/

And now, of course, we have http://aaplinvestors.net/stats/iphone/applewatchdeathwatch/

Do you start to get it? At least a little?

THE MARKET HAS NO IDEA HOW APPLE, THE COMPANY, WORKS!

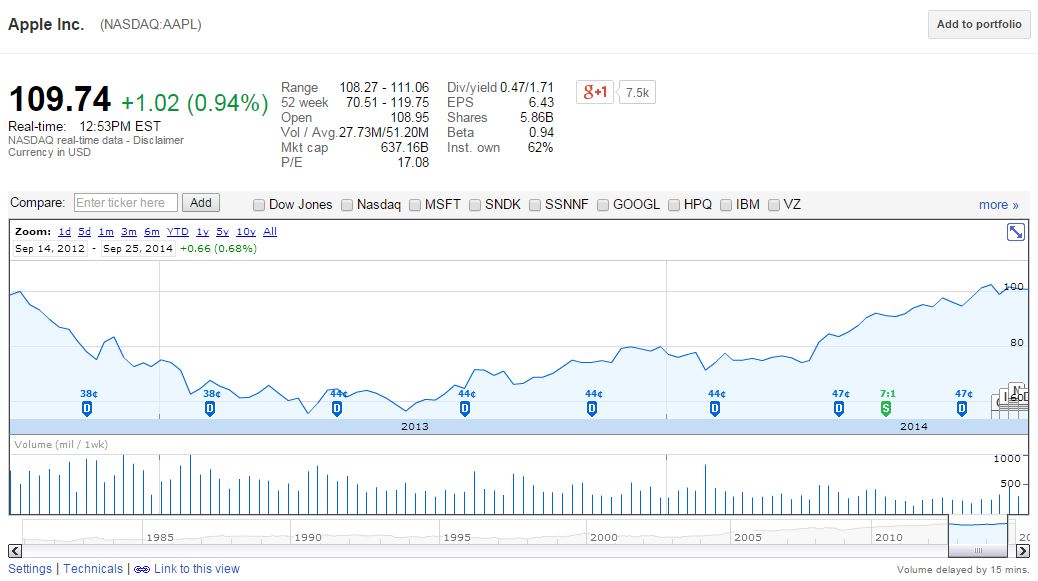

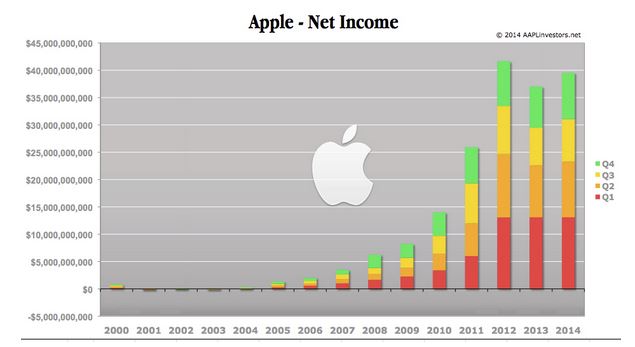

Now, look at this graph:

In two years, Apple crashed 50% and went up 100%. And this isn’t some kind of startup: it’s a MASSIVE company whose valuation was halved by half for ABSOLUTELY NO REASON! For those who don’t remember what was going on at that time, well, basically, nothing was going on. There were no bad news, no omnious signs, not even the slightest hint of a bad news. In fact, Apple kept posting record earnings after record earnings! Look:

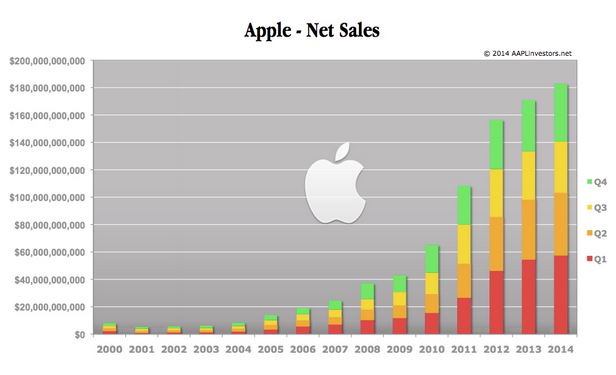

http://aaplinvestors.net/stats/

Do you see a 50% drop in sales in 2012 or 2013? Yeah, I thought so. But what about profits?

http://aaplinvestors.net/stats/salesincome/

Do you see where I’m getting at? There is no “massive drop” in profitability neither; in fact, 2013’s profits was a whopping 10% lower. So why did the stock crash 50%? How can such a large company see its stock plummet? At $55 a share, Apple was trading at a post-cash P/E of 6. We are talking about $300,000,000,000 vanishing for no reason! The market completely dropped the ball on this one.

So no, the market does not anticipate stellar earnings and no, the market does not “get” Apple and, while we’re at it, no, the efficient market theory does not describe the market. Traders are easily swayed by greed and fear, and they do some idiot move. I wonder what the guy who sold Apple at $55 think today. “Wow, I am so glad I got rid of a massively profitable company trading at a post-cash P/E of 6!”

Some people are just idiots.

Okay, but the market has still anticipated strong earnings!

Not strong enough.

Analysts currently are expecting between 61M and 69M in iPhone sales. This analyst predicts 62M iphone sales. The absolute highest number I’ve found is 71.5M.

I believe Apple has sold 74M iPhones last quarter. My range is between 71M and 77M. That’s 9M more iPhones than the midrange of estimates; at the Average Selling Price of $621 (note that the ASP most likely increased as 6 and 6+ were for sale for an entire quarter, but I am being conservative here due to a stronger US dollar), that’s $5.5B in revenue that’s unaccounted for. And remember that this is in addition to the already higher revenues due to higher sales! With $67B in expected revenues (at 16.8% rise year over year), that’s a pretty big difference that is (so far) unaccounted for!

But what do I base my estimates on? Well, just read everything above! I mean, I didn’t even mention the deal with China Mobile - for the first timer, the iPhone was for sale with the BIGGEST carrier in China for the entire holidays. Even if we consider that maybe only 5% of Chinese have the means to buy an iPhone (at least the upper models), that’s 68M people. At a 50% penetration rate of that category, that’s 39M more iPhones than a year ago.

Even moreso, the iPhone was TOTALLY SOLD OUT for most of the quarter, up to the point where people had to smuggle iPhones inside the country. You know, very soon, people will stop trying to smuggle drugs and will instead smuggle iPhones!

Now, here is what I base my estimate on: technically speaking, the maximum amount of iPhones that can possibly be made in a single quarter is a limited quantity, rumored to be around 85M based on supply chain check. Now, the number is not clear: some analyst believed that number to be 58.2M a year ago. Then again, Apple is building two flagship phones now instead of it, and it recently added Pegatron to their main assembler, Foxconn. Let’s consider the absolute maximum number of iPhones that can be built is 1M a day. Remember: this includes older models as well, such as the 5C and 5S.

Now, keep in mind Apple entered the quarter with a large backlog on orders, meaning people who awaited delivery of their products. Here for instance, the expected delivery time the day after iPhone 6 were out was 4-6 weeks! Apple still exited the quarter with a large backlog of undelivered iPhones. With 91 days in the quarter, we have 91M iPhone made, give or take a few millions. Remove a few millions for possible replacements, demo units, free units to Apple employees and so on. Remove a few millions for units in transit and so on.

How much in sales do we have?

Is the 74M iPhone sold so crazy? Sure, you might consider old models, which are well in stock, but I don’t think Apple would be stupid enough not to build the iPhones people wanted (6 and 6+) where there had been a backlog even before the quarter started. I do believe that out of the 91M-or-so iPhone made this quarter, at least 55M were iPhone 6 and 6s, and that Apple sold every single one of them. In fact, I almost think the iPhone is sold before it is even actually built.

Adding in another 20M of iPhone 5s, 5c and 4s doesn’t seem all that crazy to me. Keep in mind Apple sales peak in December!

Starting to understand my trade little?

Okay, but even if Apple posts a beat, the stock might not rise…

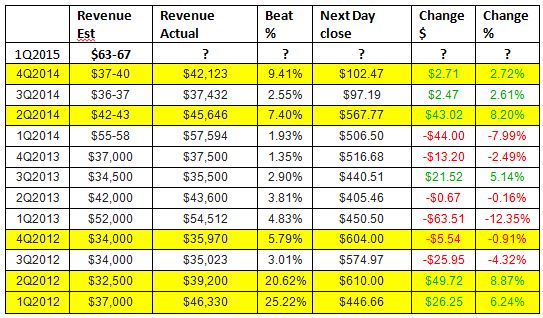

Absolutely - and this point is covered more in details later. For now, let’s look at how Apple’s stock has fared the day after earnings:

In this table, I’ve highlightened every quarter in the last three years where Apple beat its guidance (or the midrange of its guidance, when applicable) by at least 5%. Please keep in mind Apple peaker on September 28th, 2012, right as Q3 2012 earnings were out, and that Apple was trading at $98.15 per share, which isn’t much lower than what it is today (a 10%-5% dividend=5% return in 2 years while revenue are massively up? Yeah, makes sense).

Basically, when Apple beats its guidance by a significant amount, and if you’ve been reading so far, I surely think Apple will beat its own guidance by a significant amount, the stock rises the next day. Keep in mind this is the “closing” change, and that Apple sometimes even goes higher during the day (or in the afterhours market).

A 5% beat over the midrange of its revenue guidance would place its revenues at $67.73B which at this point is basically 99% sure. Hell, a 10% beat over the midrange of its guidance puts it at $70.95B. Remember that those “9M” extra iPhones bring in $5.5B in extra revenues over what the street expects.

Analyst’s consensus is currently at $67.32B, with the lowest estimate at $65.01B and the highest at $74.27B. My own revenue estimate is at $72B, range $70B-$74B, thanks to far stronger iPhone sales.

I suppose this is where you keep your “ace in the hole”

Yes. Believe it or not, there is MORE. I mean, had we left it at what was written above, I would certainly have taken a small call position, but never something as big as what I did. So why exactly did I take some a gargantuan position in a stock?

Here’s the ace of the hole:

The buyback program

When its stock was (unfairly) beaten down, Apple spent a fortune to buy back stocks. It even went as far as borrowing - twice - to do its buyback, a very, very smart move by a very, very smart CEO. Why?

Most people today, even professionals, completely misunderstand share buybacks, so I will try to explain correctly: a share buyback is one of the best thing a CEO can do to prop up the stock of the company.

It’s simple mathematics. If you earn $100 buy have to pay 100 people, each person gets $1. But if you only have to pay 90 people, each person gets $1.11, despite you still making $100.

So far, and excluding the recent quarter (in which Apple bought back even more shares), Apple has bought back $68B in shares. As AppleInsider stated it:

“Beating stock manipulators at their own game”

As a result, Apple’s number of outstanding shares went from 6.581B on March 30, 2013, to 5.866B on September 27, 2014, a 10.9% decrease. What does this mean in clear terms? It means that if Apple NEVER, EVER grew again, with a total net income of $39.51, its yearly EPS would go from $6.00 to $6.74! That’s right: Apple managed to make a yearly $0.74 per share of profits out of nowhere.

From a financial point of view, stock buybacks have a null effect on the value of a company. After all, cash that you spend buying back share is cash you can’t invest in your company. However, at the same time, Apple bought back shares when they were far too low, which is hugely profitable for shareholders because future profit per shares will come up due to this decision.

Oh, and its cash reserves are still at a record $164B. And I haven’t even talked about the dividend program yet (don’t get me started on the dividend program), which is also fabulously genius.

Now, do you start to understand?

One last thing

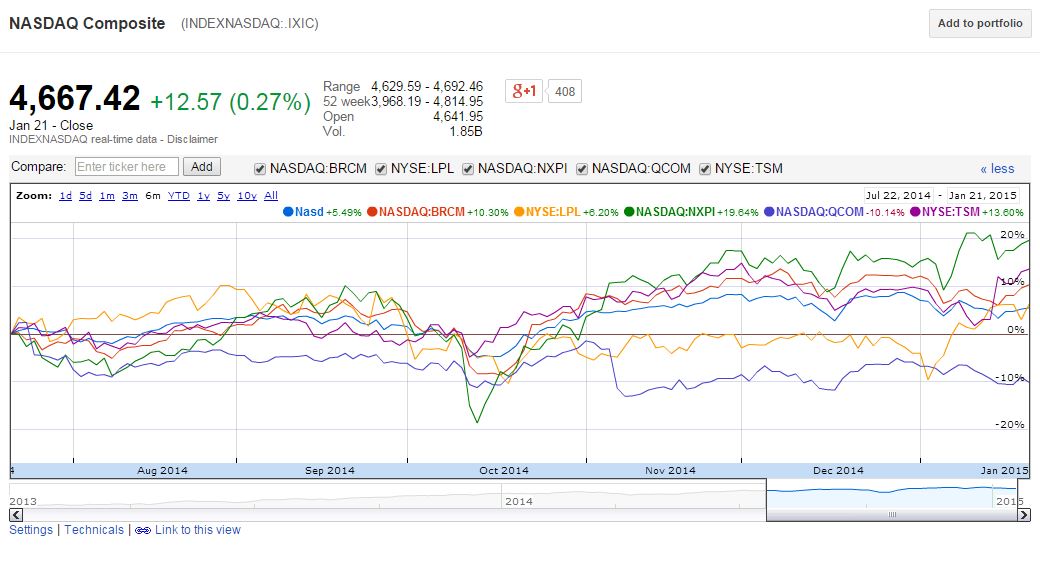

Or one more thing, as Steve Jobs would have put it. A good way to estimate iPhone sales is to study the earnings of companies that build iPhone or Mac components. Let’s look at them right now:

First, I have taken a six-months period because manufacturing for the new iPhones begin at the end of autumn (this is when the very first leaks do come up). Since sales in April-May-July are going to be reflected at the mid-July earnings report, and since Apple will increase its order for iPhone6 and 6+ componment shortly after release, this looks like a decent period to compare different manufacturers of iPhone components. This is not an exact science and these companies certainly have more than one customer (especially big guys like Samsung), but overall, it gives you an idea of the health of the market in general. In blue, that is the line slightly above “0%”, we have how the NASDAQ has fared, on which most of the companies above are listed. In the first graph, we have, in order:

- Broadcom, which manufactures different chips, amongst other things a touchscreen controller

- LPL, or LG, which manufactures iPhone screens

- NXP Semiconductors, or NXPI, which manufactures several chips, most notably the radio chip

- Qualcomm, which manufactures the 4G LTE modem

- Taiwan Semiconductor Mfg, or TSMC, which manufacture the A8 microprocessor

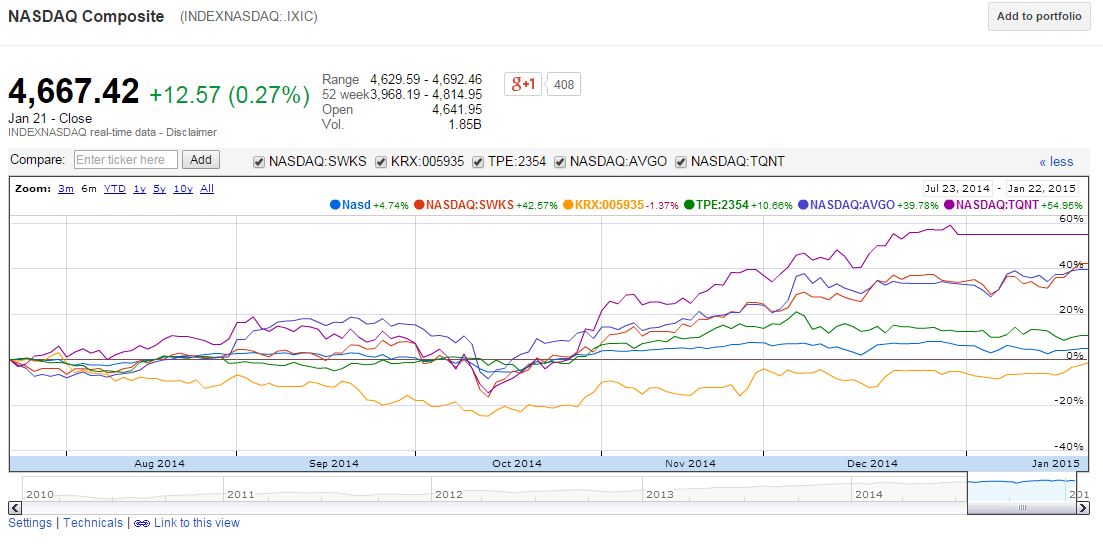

In the second graph, still with the NASDAQ, we have:

- Skyworks, which manufactures chips inside the iPhone

- Samsung, which manufactures part of the ram, screens, etc.

- Foxconn, which assembles the iPhone

- Avago Technologies, which makes some other chips

- TriQuint, which makes even more chips - it recently merged into a new company

Now, again, those companies have more than one customer - but can we agree they are doing really well? As in, much better than the overall market? If you look at earnings report from those manufacturers, guess what, many are posting record earnings.

Based on all that, and based on the fact those iPhones are not only built, but sold (still on backorder in several countries!), I am fairly confident the iPhone has done phenomenally well.

I rest my case.

So, it’s all roses and daisies and ponies?

HELL NO!

And we are entering the painful part of my position. Had I stopped at only what was written above, I would have remortgaged my house and pawned out my own internal organs to invest more in Apple.

“By my own models there is a 30% chance that I will lose 50% of my investment or more”

That’s right: you read that right. There’s a 30% chance for me to lose $15,600 or more. In fact, it happened to me in the past. I have had losses in the tens of thousands.

Imagine rolling a dice and if you get a 1 or 2, you lose $15,000

That’s the situation I am in right now. In investing, there is no such thing as a guaranteed return above the risk-free interest rate. IF ANYBODY EVER GUARANTEES YOU A RETURN OF OVER 2% A YEAR, IGNORE HIM TOTALLY. That kind of thing simply doesn’t happen. To make money investing, you have to take risk, period. You can mitigate, manage, hedge or otherwise live with the risk, but the fact remains that my position above is incredibly risky.

“Even if everything I brought forward here fully materializes, even if Apple reports a trillion in revenue, I might still lose the entirety of my $31,800”

Why? Because that’s how options are.

Let’s say Apple report outstanding earnings, but for some reason, the stock only rises to $112. It then stays there until February 20th. Congrats! I just lost $11,200! Even though the stock went up! Why? Because I paid $3.12 for something that is going to be worth only $2 ($112-$110=$2)

With stocks, as long as you invest in ultra-solid companies that are well-managed, even if the stock crashes, you can make it back the vast majority of times. I’ve had stocks I was sure were excellent that went from $50, to $40, to $60 and then to $80. Hell, I had stocks that went from $10 to $2 to $15 within two years. Sure, a stock may crash and never recover (see: Blackberry), but the fact remains that, with stocks, in general, the time is on your side.

All in all, over a long enough period of time, the stock market will go up 6-10% per year on average. If you have a diversified portfolio and rebalance correctly, you do not stand much chance of incurring significant losses over an extended period of time. But with options, you do not have that luxury.

Let’s say Apple falls to $106 after earnings, then rises to $109 on February 20, then rises to $1,000 on February 23th. Despite investing in a winning stock, I will have lost 100% of my investment!

Based on that premise, my investment is incredibly risky.

Even worse, even if Apple does report stellar earnings, systemic risk might get me!

This is the point on which I spent the most time, especially last week-end. If the entire market falls 5%, which has definitely happened several times in the last months over the course of a few days, I will be wiped out or almost wiped out. If Apple falls, my options lose most of their value, so even if Apple was to blow out expectations, if the entire market is down, my options are toasted.

Indeed, my investment horizon is short - not even a week, now. Still, last week-end, I have identified six potential important risks that could make me lose everything.

The potential problems

1) China GDP slowing down.

I was worried, up to a high point, about the 2014 GDP growth number in China. Analysts expected 7.3%, down from 7.7% the year before and 0.2% below Beijing’s official target of 7.5%.

A very low GDP growth report might have set market panic and caused a drop in the market. However, the number came in right in time and a little bit above what analysts expected, at 7.4%. This opened the possibility of the trade for me

2) ECB’s QE program and falling euro

This was by far the biggest question mark in my plan. As many may know, ECB, the European Central Bank, is about to announced a Quantitative Easing to stimulate the economy of countries in the European Union. This program has been expected for quite some time now, and should it disappoint investors, the entire market could crash significantly.

The latest rumour, out today, state that the ECB is going to buy buy $5B euros of bond per month until… Until, until. This is one excellent way to fight inflation and help the economy and, given the market reaction today, one would say the ECB would be deliveringpretty much what everyone was expecting. This kind of Quantitative Easing work: just remember that’s what the Fed did and while it’s hard to attribute the economical growth in the US to a factor in particular, one might claim it worked pretty well.

Now, I had to take my decision even before the rumors were out, and it was quite a risk. At the end, this is something I accepted to live with. For instance, should the ECB announce it isn’t going to do anything after all, I will incur a very significant loss. Now, to be clear, I am not totally in the clear yet: a rumor is a rumor, and the QE might end up being something else entirely. Also, investors might be expecting even more and have a delayed reaction, or something else could go wrong. Overall, I do believe that the odds of a correction stemming from this idea are much lower today than they were a month ago.

3) Greece elections

On January 25th, two days before earnings are release, Greece will have another election, and the extreme left, Syriza, is mostly going to win. This may mean Greece will leave the European Union, and this may mean the European banking system will crumble. However, I do believe this has long been accounted for, and I do believe that Greece will not exit the European Union, which would be a total catastrophe for them. I do not think Germany is going to let that happen. Should Greece default on its loans, banks in the EU will incur massive losses that may spread a massive financial crisis. However, since the last Greek crisis, certain measures have been put in place to prevent that kind of contagion. The problem, in my mind, is very different than it was three and four years ago.

Still, a strong left party could rattle the market and cause a panic monday at opening, making me lose my entire investment.

4) The Swiss Franc debacle

Last week, the cap on the Swiss Franc was removed. Basically, in the past, SNB, or Swiss National Bank, guaranteed that an euro could always at least buy 1.2 Swiss Franc. So in short, if you are paid 1,000 euros a month and live in Switzerland, where everything is in Swiss Franc, you were guaranteed a minimum of 1,200 Swiss Franc a month.

But not anymore. Your 1,000 euros a month would now be worth 1,000 Swiss Franc a month, a massive difference. For those who don’t follow the market, this caused a massive panic and several bankruptcies, even amongst some of the top brokers. Right now, you have to PAY to hold Swiss Franc with some brokers, a negative interest rate.

This action caused extreme volatility whose effects are far from totally understood and visible today. Several european banks who were shorting the Swiss France face massive losses. This is still something that could ruin my position and options trade.

5) Various growth indicators

Several important indicators on the state of economy are awaited this week - manufacturing, housing, confidence, etc. A bad indicator might spark a selloff and given my trade, this could very well wipe me out completely, even if it barely lasts a few days or week.

6) Earnings of other companies.

We are in full swing of the earnings season, with many companies reporting in and strong profits and revenues expected. Already, banks have disappointed massively, causing another drop in the market last week. But what will it be this week? I had to make a call on it, and I decided that since everything indicated earnings would be strong, I had no reason to seriously worry. Furthermore, excellent Intel earnings comforted me in my decision to go ahead in the trade.

7) A hedge fund liquidating its Apple position

Honestly, when you have a company as big as Apple, few things can move its stock price significantly. Even if everyone who read this sold $1,000,000 in shares of Apple, the price would barely budge. Hedge funds and big investment funds are the only ones with the power to crash Apple, and they have done so in the past, like with many other companies. This was one of my primary fears: that Icahn (who owns a significant portion of Apple) or another started dumping his shares pre-earnings. This would cause the price to plummet and even if Apple recovered later, it would be too late for me.

At the end, I decided that if a hedge fund was going to sell, he mostly was going to sell before the end of 2014, for taxes and annual return purposes. Apple being lower than its 52-week high, my thought process was that if a hedge fund wanted to sell, it would have done so already. Also, this is a double-edged sword: those funds might very well buy post-earnings as well. Overall, this is another massive risk, even if everything in my theory is proven to be right.

Do you plan to sell your options pre-earnings?

No, I do not plan to do so.

There are a few exceptions, of course, and a few situations where I would sell my options. One of them would be if Apple appreciated significantly before earnings are released, or even before the close on the day of earnings. I have a target price that, once reached, will cause me to sell half my position, another one that will cause me to sell another half, etc.

Why a February 20th, 2015 call? Why not a January 30th call if you want to play the earnings?

Someone brought this point in the Reddit thread and I have to say this: he is right.

With earnings out on the Jan 27th, I would still have Jan 28th, Jan 29th and Jan 30th left as trading sessions. At the time I took my decision, Jan 30th calls were about $0.80 lower than Feb 20th.

I took my decision to buy Feb 20th calls based on five factors:

- Higher volume for regular options (Jan 30th is a weekly option)

- Less chance to get squeezed; I cannot exercise my 10,000 options, which would cost me $1,110,000, and I might thus be unable to fully reap the rewards of my position

- I don’t like plays that are so far from expiration. With only three days left, buying Jan 30th was far more risky (in terms of %) with less manoeuver room

- Finally, even if the earnings come in “great” but not “WOW,” I will have some room, and will lose less money because my options will not be mere days from expiry.For instance, if the stock rises at $112 after earnings, there are good chances I will get almost all of my $31,800 back, due to the fact there are three weeks left until expiry (with some loss on the vega, as some have pointed out)

- … and, lastly, the Apple Watch. Now, let me tell you this: this one is going to be absolutely amazing. Sure, it’s due in March, but leaks begin before that. I fully expect the “hype” of the Apple Watch to start in early-mid February, and this could prove a boon for my Feb 20th calls.

Why not hedge your position! You are way overexposed! Sell some $115 calls

I have considered the idea of a spread in detail. Were I to sell some $115 calls, at least I would recoup a portion of the premium I paid for the $110 calls.

But at the same time, I am severely limiting my upside if Apple has a blowout report and soars higher, which is my belief is what will happen.

Why not sell puts instead?

Because when you do that, your maximum profit is capped at the premium you obtain for the put. Make no mistake: it’s a smart move and another way to profit. Someone recommended me to sell some 95 puts and buy some 90 puts, a put spread. This is a good idea and, again, I insist that this person is smart and knows what he is doing.

But with that kind of play, your maximum profit is capped at the premium of the $95 strike put less the $90 strike put. This is far from stupid and an excellent strategy as well, but it’s still a very different way to play this situation.

How are you feeling right now?

How would you feel? I am extremely tensed up, anxious, I check my stocks every five minutes, and I already prepare myself mentally to the thought of losing $31,800 just in case.

This sounds so cool! Should I do the same thing as you and buy Apple calls?

NO!

Do NOT do what I am doing here! 95% of people who will read this text will fail to realize just INCREDIBLY RISKY my play is here.

In fact, let me make this clear: there’s a good chance I’ll wake up Wednesday, January 28th, and will have lost $20,000+ USD. This isn’t a fairy tale, this isn’t a story where the good guys (me) always win, this isn’t a joke, this isn’t a “yeah, there’s risk, but not really,” this isn’t a game, this isn’t nice story written by cool people, it’s finance, and it’s very, very, VERY possible I will incur MASSIVE losses from what I have done.

Watch this

“Are you sure you want to make this bet with your life savings?”

“Yeah. I’m certain.”

This isn’t a joke or a show. This man could have very well lost his entire life savings. In fact, the odds were against him. Now, I’m not betting my life savings, and even if things don’t work out, I might lose less than my entire original investment, but the fact remains that NO, YOU SHOULD NOT DO THAT.

Buy stocks instead. Or do the put strategy described above. But no matter what you do, do NOT do the same thing as me unless you 100% understand everything I just said, and even there, don’t do it.

Final words?

As I write this, I still have no idea what will happen. There is something quite… exhilarating about the entire thing. Maybe I will come back to this thread mourning all the money I lost and calling myself an idiot for “not seeing something obvious” or something like that. On the other hand… On the other hand, maybe I will come back and celebrate that key moment in my life that defined me as a person

I know what’s going on. I know the trade I’m in, I know what might happen and I am not backing down.

No question, just wanted to say you are insane, but good luck!

Thank you, and remember my favorite motto when investing: YOLO.

One problem with your premise is everything not related to AAPL. If you look at the charts of VXX, it is heading for a potential golden cross. VXX only golden crosses when the markets are at peril. If the markets settle down and VXX falls appreciably, then individual names like AAPL stand a better chance of rising with less risk. However, VXX has been elevated which means something nefarious is in the works related to the overall markets. If something happens to the Chinese Yuan, or Greece is forced out of the Euro zone, or oil drops to $25 /barrel….one or some combination of these events seems to be getting primed to happen and will likely take the market down with it.

My point is that the VXX is elevated, getting ready to golden cross and this almost always means the market will experience a correction. Continue to watch the development of VXX, it is signaling that there is danger lurking in the overall markets and it has my attention. Any major investments like yours is one major news story away from being wiped out and VXX seems to think that news story is getting ready to happen.

Man, that is one of the greatest investment bets I’ve ever seen. Hats off to you, I will be crossing my fingers it comes off for you!

You did it! Congrats buddy, there’s no way I would’ve had the guts to hold that position but you nailed it. Enjoy the $$$!

congrats! i hope you cover some tonight or tommorrow, its always good to take some risk of the table and sleep well again !

Congrats! I hope you take some of your profit of the table, So you can sleep well. If you want to continue the trade keep 25%

Very ballsy move on your part, and from the early signs of things it looks like the right bet! Up to 116 in AH. Good luck to you and I hope its even higher when they expire.

Hell yeah man congrats. Hard work pays off; you’ve earned it!!!

Just awesome. I’ve followed you for awhile now. Happy to see you get a win here.

I’d assume you made at least past your first exit point, hope it carries on towards 120 for you.

I agree