The rise of the US Dollar creates an incredible opportunity to invest in foreign markets. While nobody knows for sure just how strong the US Dollar will get (it currently sits at $0.82 USD=$1 CAD and it used to be at $0.60 USD=$1 CAD around a decade ago), I do believe now is a great time to start investing in international market, especially Europe and Canada. Remember that countries that export to the United States gain from a strengthening US Dollars, and vice versa (US companies selling in Europe, such as Apple, are negatively affected).

I have always believed in the importance of investing in more than one market. If you think about it, Canada is a kind of mini-USA: think of it as a less extreme, less polarized country. Canada doesn’t have all the super schools, the super cool Army full of soldiers with next generation weapons and the razor low personal income taxes, but at the same time, it doesn’t have all the violence and guns, the Patriot Act and the NSA (although the CSIS is giving them a run for their money). For those reasons and many more, I do believe Canada is a great country to invest in.

Without any further delay or half-bigoted, half-formed opinions on the United States, here are three Canadian companies I believe should be in any investor’s portfolio, no matter where they live. These companies have been hand-picked for the incredible performance and growth opportunities. On a risk-adjusted basis, they offer an outstanding growth profile, both in terms of market value and dividend. Amongst all Canadian stocks, I consider them the “best of the best” and from a long-term investment horizon point of view, it will be extremely hard for you to lose money on those; in addition, they all offer a very attractive dividend yield that is quite safe and expected to grow at a pace faster than inflation over time.

In other words, get paid to wait with these awesome companies.

Contents

3) Whitecap Resources - TSE:WCP - 5.32% yield

When it comes to investing in oil and natural gas, this is the company you want to have in your portfolio. Whitecap Resources is one of the safer Exploration & Production oil companies in Canada, while also offering excellent growth opportunities, a conservative balance sheet, outstanding hedges as well as a very sizeable dividend. These days, when it comes to oil, nothing seems certain anymore, but WCP is certainly amongst the safest companies, just millimetres below Suncor, Enbridge and Imperial Oil. However, unlike these maturing companies, WCP offer a far better interesting growth profile as well as a much more attractive dividend (and possible dividend growth, when oil finally recovers).

WCP has excellent hedges in place for the reminder of 2015 and most of 2016. Furthermore, its balance sheet is extremely solid and the company’s debt is very manageable. Unlike several Oil E&P that got excited and started drilling everywhere, WCP is very conservative when it comes to its Capex. Furthermore, given its low BoE cost, it will be one of the last to crash in the Oil & Exploration market should oil weakness persist. Its BoE cost is somewhere around $12, way below average and still affording the company way more than enough room to pay for all its expenses and dividends. Furthermore, keep in mind WCP operates in Canadian Dollars, as in, it pays its employees and machinery in Canadian Dollar. That’s a big, big advantage that is rarely discussed. At a WTI of $55, with an exchange rate of $0.82 and with a (very pessimistic) $10 rebate on WTI, WCP is still selling its oil at $35 a barrel, far above its production cost. Even if oil should fall further, remember the impact of a lower Canadian Dollars will at least partially compensate that fall.

To give you an idea, WCS (Western Canada Select) currently goes for $52.63 CAD, far above a level that could be considered critical

Management

Whitecap Resources’ management is legendary. Amongst all oil companies in Canada, WCP’s management is certainly in the top 3.

Even after the current crash in oil prices - with projects being slashed left and right and profits falling through the floor - Whitecap Resources somehow manages to not only pay out a 5.5% dividend, but to have a positive free cash flow as well. I do believe those are funds that could eventually be used for acquisitions, specifically, of troubled shale oil and gas projects.

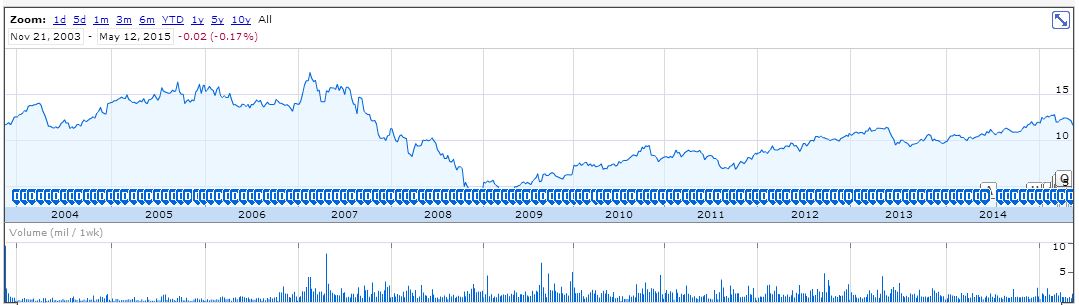

Look at this beautiful graph:

Did oil crash in late 2014? I can barely see it on the graph. Looks like normal volatility to me.

When every oil company was slashing its dividend left and right, WCP was keeping the cap, to say the least, and I am convinced dividend rises will resume as soon as oil recovers.

Balance Sheet

WCP’s balance sheet is outstanding - not as solid as Suncor and Enbridge, but not far behind neither. Inches behind.

There is not even the slightest risk of a dividend cut at the moment and the company is well positioned to sustain a prolonged oil barrel drop. It will be amongst the last “medium-cap” oil companies to fall in Canada, should it come to this (which I don’t think it will).

Final words

WCP will allow you to benefit from oil’s recovery, while still handing out a generous and quite safe dividend. Their dividend would be at risk should oil fall below $35; however, again, this is sort of counterbalanced by a weakening Canadian Dollar. Again, when the CAD and USD were at parity, a $80 WTI meant a $80 Canadian per barrel; with the Canadian dollar now at $0.82, a WTI at $55 means getting $67 per barrel, which isn’t all that lower than a mere year ago. Canada’s barrel of oil is also going through the roof, up 77% since hitting its bottom at the beginning of this y ear. All this to say canadian Oil and Gas Exploration & Production companies have overall held better than their american counterpart.

Unless you are extremely bearish on Oil, which you shouldn’t be, this company belongs in your portfolio.

Alternatives

TSE:ARX is pretty much a WCP copycat with a slightly higher risk but equally as competent mangement, TSE:HSE is slightly less good than WCP and pays a slightly smaller dividend.

2) Chartwell Retirement Residences - TSE: CSH.UN - 4.72%

The legendary seniors housing company and perhaps the least risky company I can think of, Chartwell Retirement Residences is such a good investment I have considered going into politics to make a law banning investing in it. Why? Because it’s such a good investment that it’s almost unfair for those that choose not to invest in it. When people google “ultra-safe dividend,” they should see that company at the top. Unless a new supervirus comes out and starts wiping out everyone older than 65, this dividend will keep coming until the Apocalypse comes.

Chartwell is renowned for offering mid-quality, mid-priced senior housing, something that is not obvious to do, not easy to imitate and almost impossible to successfully replicate. Simply said, a patient’s relationship with his medical personnel is something that does not appear in any financial statement, yet is almost invaluable for the long-term prosperity of a company.

In fact, look at this beautiful little baby:

Isn’t that the most beautiful thing in the world? A constant stream of dividend that never, ever ends. Free money being sent to you every single month! Sure, the company cut its dividend during the financial crisis and it could be argued the stock is stuck in a narrow trading channel, but the fact remains that Chartwell is a superb company that is significantly undervalued right now and offers you a check every month for very little risk.

For the low risk it offers, it’s well worth an investment

Management

Chartwell’s approach to offering housing to seniors is refreshing. Unlike some other companies that are obsessed with profits and profits alone, Chartwell is dedicated to offer a better living environment to its residents. While this may create a lower profitability for us shareholders and investors, I do believe this attitude to be the right one on the long term and here’s why. Every day, it seems that you hear about yet another seniors residence abusing its residents. Now, unlike news about children being abused that pretty much no one cares about, people do raise hell when seniors are abused. In a way, you’ll never be a kid again so why would you care that some moron somewhere is beating his children? That will never happen to you anyway, right? However, when it comes to seniors being abused at a home, well, this is something that might happen to you, so I guess people care more.

That kind of stories lead to bad press, lawsuit and a myriad of other bad stuff. Would you place your parents at a place that was caught raping their residents? Yeah, thought so.

Notice how you won’t find “Chartwell” anywhere in these articles, ever?

Then again, I guess people don’t care. I mean, where else can you dumpyour parents when they become incontinent? It’s not like you want to take care yourself, so how many care about a 0.1% chance of their parents getting sexually abused at a seniors center? Many will say that they do, sure, but at the end of things, the majority will look at the center that’s the cheaper. Maybe my approach of “invest in seniors housing that treat its patients well” isn’t the right one. I don’T know.

Anyway, Chartwell is a center that really cares about its residents and I like that. It’s not amongst the highest-quality (that would be Amica), but it’s not far behind, and the price is much more reasonable. Chartwell is an excellent company led by an experienced, veteran team and is poised to thrive for the decades to come.

Balance sheet

There is no real balance sheet risk with a seniors housing company that doesn’t actually abuse its residents except perhaps for the risk of being overleveraged (i.e. borrowing too much to acquire too many centers), which is not the case here.

There is nothing to be worried about in Chartwell’s balance sheet.

Final words

With a strong dividend that has only one way to go (that is, up), CSH.UN is an excellent long-term play on senior in Canada. With pricing power and pretty much a co-dominant position in Canada, this is a company that is borderline invincible. With an ageing population, Chartwell’s future is bright and I consider it one of my top defensive investments.

Alternatives

TSE:LW is excellent and offers a higher dividend for slightly more risk, TSE:ACC offers a higher dividend for lower growth opportunities.

1) Brookfield Infrastructure Partners - TSE:BIP.UN - 3.93% yield

… and we are now at the top! A company that is actually hard to invest in due to its L.P. status (Interactive Brokers won’t let me invest in them!), this is pretty much a godlike company. This company is so good people will one day start worshipping their management and erecting pyramids in their name. In fact, the legends says a book was missing in The Bible, and that book was about Brookfield.

If I had to sum the company in one word, it would be this one: perfection. This is a company that can neither be slowed down nor stopped.

“See ya, bro!”

What is Brookfield? I’ll let the company’s management sum it up for you. I consider the following paragraphs to be among the most beautiful and sexy ever written:

Brookfield Infrastructure Partners L.P. operates high quality, long-life assets that generate stable cash flows, require relatively minimal maintenance capital expenditures and, by virtue of barriers to entry and other characteristics, tend to appreciate in value over time.

There we go. Try to write a more beautiful sentence and come back to me. Let me try:

F.S.Comeau Inc. seeks to maximize profits while minimizing losses, optimizing returns and transcending the limits of modern investing with extraordinary investments in godlike assets with ultra-low costs and exceptional growth, phantasmagoric profitability and almost negative risks.

Not bad… Not bad at all. I would really have a career writing that kind of stuff.

Management

Brookfield’s management is extraordinary at finding and buying assets, as well as fully developing them. I don’t even need to tergiversate here: they’re amazing, outstanding, godly, etc.

Really, what do you want me to say here? Brookfield’s management is legendary and pretty much the de facto standard when it comes to “sucessful investments.” Just look at all the awesome assets they have.

Balance Sheet

BIP.UN’s balance sheet it so solid it could be used as a standard for all other companies to be compared with. It’s so solid that it would take 10 financial crisis in a row to start damaging it and even there, not by much. As long as people will need roads, bridges, electricity, energy and building, Brookfield will thrive.

Final words

Brookfield’s dividend is going up so fast that you might not be able to keep with it. It is typically increased 10%-12% per year and I do not foresee any end to that trend. In fact, over the last few years, it has gone up by a compounded 13% annual growth (!). Yes, that’s how good their management is. With inflation, your dividends get an “automatic” increase simply because BIP.UN raises its rates every year.

The stock is super expensive, but think of it as buying a nice car - a Ferrari or something. Except your Ferrari appreciates in value every year and sends you a check every 3 months.

This is an investment you will bequeath to your grandchildren. It’s so diversified and so amazingly-managed that you will never want to sell it. Again, this is an L.P. and it’s quite hard to invest in it, but when you do, your entire life will be better.

Alternatives

I don’t see why you would need an alternative, but BAM.A - BPI.UN’s dad - is also quite solid, yet with a smaller dividend. Aside from that, there is nothing, to my knowledge, that offers such a diversified and outstandingly managed investment as BPI.UN.

TSE:EMA and TSE:VNR are both excellent, but not nearly as diversified nor well-managed as BPI.UN. They’re both excellent investments, however.

Conclusion

Canada is awesome. Good investing!

No comments yet.