I have been dazzled by DWTI’s apparent invulnerabillity to time decay ever since I’ve started trading it. Since it’s a triple leveraged ETF product (meaning it seeks to go up 3% for every 1% ), it HAS to go down on average. In other words, this product should slowly see its value erode through time. Yet, DWTI seems to hold strangely weird over time:

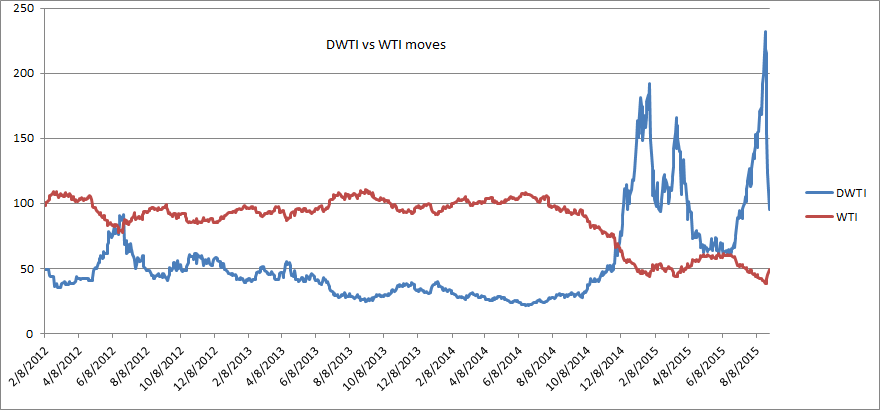

To study what decay DWTI had, and whether it was worth trying to benefit from it, I did a graphical analysis of DWTI vs WTI based on every close price from March 9th, 2012, to August 31th, 2015. Here are the results:

Again, the decay seems almost absent, at least from this graph. Over such a period, I would have expected DWTI to lose pretty much 50-60% (or more!) to decay, yet it seems to track WTI moves (amplified by a factor of 3 as this is a triple leveraged product) pretty well. If that was correct (i.e. no time decay), then buying both UWTI and DWTI would basically be a way to print “free money” as someone could basically buy both and just wait, with any variation in the underlying yielding strong profits.

This little segment of DWTI’s prospectus had a few ideas:

Therefore, there should be a slow decay in the underlying value of the fund. For instance, say WTI and DWTI both trades at $100 today. WTI goes up 10%, to 110%. Thus, DWTI would go up 30%, to $130. But now, WTI goes down 10%, to $99. DWTI would thus go down 30%, to $91. Although WTI overall fell by 1% from $100 to $99, DWTI fell fell $100 to $91, a 9% drop. And that’s even considering rolling costs, management fee and possible contango effects on the futures prices.

Therefore, there should be a slow decay in the underlying value of the fund. For instance, say WTI and DWTI both trades at $100 today. WTI goes up 10%, to 110%. Thus, DWTI would go up 30%, to $130. But now, WTI goes down 10%, to $99. DWTI would thus go down 30%, to $91. Although WTI overall fell by 1% from $100 to $99, DWTI fell fell $100 to $91, a 9% drop. And that’s even considering rolling costs, management fee and possible contango effects on the futures prices.

So, what gives? To figure out the answer, I calculated DWTI daily returns over the same period, dividend them by three and took the negative value of it (as DWTI is bearish and, thus, moves in the opposite direction). Here are the result:

The table is as folllow:

- In column WTI%, we have the percentage move of the WTI (Western Texas Intermediate) at the close of the day, from the price at the close the day before. We expect DWTI to move roughly three times this amount, in the opposite direction (i.e. go down when WTI goes up and vice versa)

- In column EMDWTI, we have the Expected Move (EM) of DWTI based on the variations of WTI (preceding column)

- In column AMDWTI, we have the Actual Move (AM) in DWTI. For instance, in the first line, DWTI went down by 19.68% on August 28th when it should have went down 19.92%

- In the “Diff” column, we have the difference between the Actual Move and the Expected Move. A positive number is good, menaing our product overperformed its objective.

- In the sum column, we have the multiplicative sum since March 9th, 2015, of the difference. Since a positive difference is bad and we use a simple multiple sum, a lower number means the product failed to achieve its objective.

- We end our data set with a sum value of 81.67%, meaning DWTI failed to follow its objective. To be more clear, WTI fell 48.77% during this period, meaning DWTI should have gone up 146%. It instead only went up 87.23%.

We also come to the following conclusions:

- Due to the very nature of the product, some anomalies will be present. For instance a pure triple leveraged product would mean a 33% rise would lead to a 100% drop in the ETF. However, DWTI and UWTI are designed not to hit 0 (else the managers stop getting paid!)

- DWTI is kind of seen as a forecasting tool and, sometimes, “anticipates” or “catches” what people expect to happen to futures. Obviously, futures and DWTI attract very different traders and sometimes, the imbalance in the buying/selling sides can create anomalies.

- DWTI is exceptionally exposed to a huge rise in oil price and would plummet “in a moment” should oil rise again.

- The true decay is probably hidden given the period chosen (oil crateauing 48.76% over our period while DWTI is only up 87.23%, far below the 146.28% it should be.

- In our view, shorting DWTI when oil is extremely low is an extremely efficient way to play an oil rebound with a minimized risk and a very strong probably of a 100% gain.

- With WTI at $42, we estimate that a simple rise by 33% to $56 will wipe DWTI below the $10 mark.

- On the opposite, UWTI was at $34.67 when WTI was at $96.03. It now stands at $1.07 with WTI at $44.16. Even if WTI recovered to $96.03, UWTI would barely increase to $3.30 or so.

- Therefore, shorting both UWTI and DWTI is an excellent way to play volatility, with a few caveats (borrowing fees, locating shares, interest rate rising, rebalancing, etc.). Shorting both the same amounts in UWTI and DWTI before the oil crash, assuming a daily rebalancing, would have yielded a 97% gain on the UWTI with only a 87.23% loss on DWTI.

- Thus, from the $5,000 spent shorting UWTI, only $150 would be left to repay. Of the $5,000 spent shorting DWTI, you would now owe $9361.5. Overall, you would have earned $488.50 over 14 months, for a grand return of 4.88% (before interest fees) on your trade strategy, ASSUMING NO REBALANCING.

- Assuming a weekly rebalancing to always keep the same shorted amount in both UWTI and DWTI, your gain would have been roughly three times as high, for around 13%, depending on the actual day of rebalancing and rebalancing method. A daily rebalancing yields even better results. Of course, these amounts exclude commission.

- Even had oil not moved, you would have made a small gain from the time decay of around 10% per year, without any need to rebalance.

- Overall, it may be better, for the risk-seeking investor, to simply play the trend, if it can be found. DWTI in particular is doomed to plummet unless oil keeps falling. A simple rise to $56, as we repeat, would wipe DWTI out completely below $1, even though WTI used to trade at over $90 for quite a while.

Based on those elements and the multiplicative error, we estimate DWTI’s decay - only from its errors in tracking its objective - to be roughly 0.03% daily, or 7.83% annually. However, this period was marked by a quickly crashing WTI and it is probable the decay is higher (much, much higher) than calculated.

Calculated decay from the realized move over the period, the annual decay is 10.39%.

I dont think shorting DWTI is a good idea for the investor looking going long oil. Buying simple futures can be a better way.

DWTI is $365.27 today (Jan 15, 2016) vs $106 on Sep 9, 2015 (date when this article was published). It means DWTI increased 244% for this period of 128 days. It means risk return ration is 1 to 2.4.

IMHO both have their advantages and disadvantages.

Shorting DWTI implies you don’t mean to roll, for instance.

Have you updated your model recently. I would love to see the results..