Navios Maritime Midstream flew under the radar. Even right now, barely anyone discusses it and from the tone of the conversation, you’d believe it’s just another overdone company become public. Yet who would believe Navios Maritime Midstream, or Navios for intimiates, is one of the largest transportation companies?

Contents

- 1 Introduction

- 2 The Good

- 3 The Bad

- 3.1 1) An IPO that is beyond nightmarish

- 3.2 2) The US imports less and less oil, reducing the needs for cargo shipment of oil

- 3.3 3) Risk of shipwreck

- 3.4 4) 100% dependent on the demand for oil, which is currently in a downtrend

- 3.5 5) Its parents are doing okay, but not much more

- 3.6 6) Risks, risks everywhere!

- 4 Conclusion

Introduction

Do you like big boats? Because that’s how you get big boats.

A ship owned by Navios Maritime Midstream

That’s a VLCC, or Very Large Crude Carrier, a boat that, well, carry a lot of crude oil. And can you believe this isn’t even the biggest we can go? There are such things are “ULCC” Ultra Large Crude Carrier. These carriers are so big they can’t even dock at a port, so they have to bring out smaller ships to take out some oil and lighten the boat.

Navios owns four of these ships. These ships are chartered, basically meaning that they are rented in nautical terms, to companies that want to move oil around. And by moving oil around, we mean delivering oil from where it’s produced to where it’s needed.

That’s it. You know everything there is to know about Navios’ business. Let’s move into the good points.

The Good

I really Navios is really one of those IPO that went under the radar; with Virgin Americas and Fibrogen becoming public this Friday, little attention has been given to Navios and its business. In fact:

The Street is starting to hear talk of a price cut to get it out the door. Nevertheless, people are said to be passing on this deal. They consider the company in the shipping industry and shipping IPOs have struggled in the aftermarket.

So, is it a little hidden gem or a catastrophe in the making? Navios is one of the latest in a string of midstream companies going public (mostly because of tax reasons), and most midstream IPOs have either declined or not progressed much. Let’s look at its good points.

1) Low IPO price.

The IPO values the company at $186.9 million at the middle of its $19-21 range. And we heard the IPO might be delayed due to lack of demand, meaning the range will get lowered. Personally, I foresee an IPO price of $20, right in the middle. I do not expect a big jump on opening and probably a small drop simply because this deal is “dead cold” and due to the fact transportation stocks are getting massacred (and oil as well; the combo isn’t that great). However, here is one thing for you to consider:

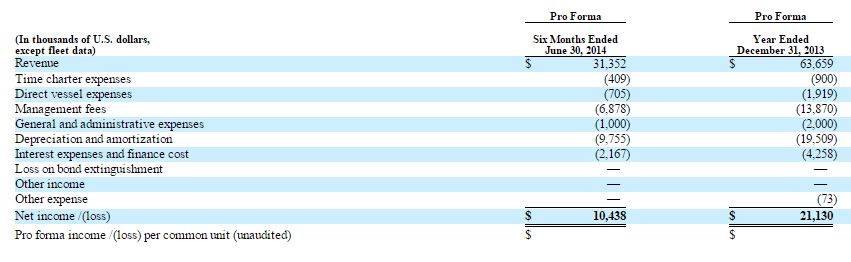

Currently, the firm earns $21.1M per year after depreciation.

Its expenses are incredibly stable; you would believe it to be a Swiss clock.. In fact, in the last three years (always pro forma, because the company is going to be a spinoff; it’s currently part of a bigger company, more on that later), all of its costs have been steadfast. Multiply the first column, which covers half a year, by two and you get very close to the second column.

So in short, you have a company that is making $21.1 millions a year and with an average chartering remaining duration (rental of its boats for transport operations) of 6.7 years, this simply isn’t going to change. How can you possibly not like this?

2) 8.25% dividend? Hum, hello?

At the middle of its IPO range, Navios Maritime Midstream plans to pay 8.25% dividend. This would roughly translate to $14 millions a year in dividends. Based on the revenues ahead, the company can easily afford that dividend. Consider this part of their prospectus:

A time charter is a contract for the use of a vessel for a fixed period of time at a specified daily rate. Under a time charter, the vessel owner provides crewing and other services related to the vessel’s operation, the cost of which is included in the daily rate and the customer is responsible for substantially all of the vessel voyage costs. All of the vessels in our fleet are hired out under time charters, and we intend to continue to hire out our vessels under time charters.

Oh yeah, their boats are “time chartered” for an average duration of 6.7 year at the moment. Not bad, huh? And do you really think they’ll have any problem renewing their chartering contract when the time comes?

Why is nobody talking about this fantastic company? Why are they talking of a price cut? Do people seriously believe they can earn more than 8.25% per year from a company with a similar risk profile? At the very least, it is worth a talk!

3) Advantageous tax treatment

Here’s a quote from its prospectus:

The Section 883 Exemption. In general, the Section 883 Exemption provides that if a non-U.S. corporation satisfies the requirements of Section 883 of the Code and the Treasury regulations thereunder (the “Section 883 Regulations”), it will not be subject to the net basis and branch profit taxes or the 4.0% gross basis tax described below on its U.S. Source International Transportation Income. The Section 883 Exemption applies only to U.S. Source International Transportation Income and does not apply to U.S. Source Domestic Transportation Income. As discussed below, we believe that based on our ownership structure after the consummation of this offering, the Section 883 Exemption will apply and we will not be subject to U.S. federal income tax on our U.S. Source International Transportation Income.

That’s the entire point of a midstream company in the first place: not to pay income taxes. In fact, that’s the entire reason for setting a midstream company and that’s pretty much the sole reason midstream IPO are invading the market at the moment: non-taxable profits.

In fact, a portion of the dividend that is paid to you is considered return of capital, and is not taxable; it does not come as income, but simply as if the company was giving you your money back. It does create a bigger capital gain when you do sell the company, however.

4) A business that is not going anywhere

It’s oil shipping. Across the sea. This isn’t something like telegraph, radio or printed newspaper, in a market that is slowly dying. We are talking about shipping a massive amount of oil overseas. This is perhaps the “most likely to never go anywhere” business ever made.

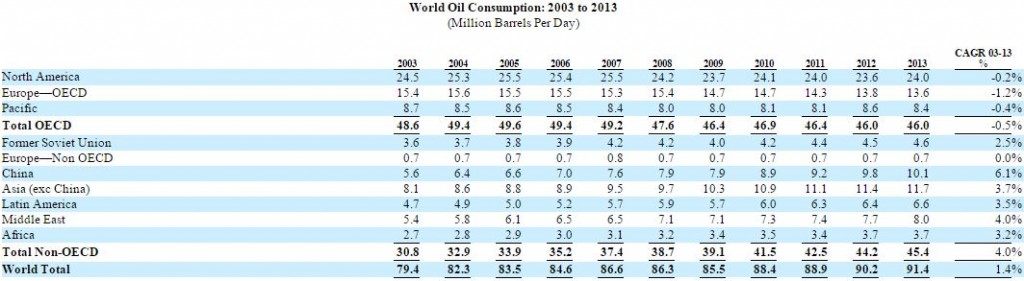

Still not convinced? Look at that:

What you should get from this graph (which I found surprising, admittedly. I expected oil demand to grow across North America) is that China’s demand for oil is quickly going up. However, China produces around 4.6M barrels of oil per day currently. Where do they get the 11.7-4.6=7.1M barrels difference? Some through its pipeline from neighbouring countries, yes, but also a good part by sea.

Navios Maritime Midstream is not going anywhere.

5) … and we have growth too!

Contractually, Navios Maritime will be allowed to buy boats from its parents at “fair market value.” Let’s look at its prospectus once more:

We will have options, exercisable for a period of two years following from the closing of this offering, to purchase the following seven VLCCs from Navios Maritime Acquisition at fair market value. Although we anticipate that we may exercise some or all of our options to purchase the following seven VLCCs, the timing of such purchases is uncertain and each such purchase is subject to various conditions, including reaching an agreement with Navios Maritime Acquisition regarding the fair market value of the vessel and the availability of financing, which we anticipate would be from external sources.

Keep in mind the entire reason for Navios(parent) to sell ships to Navios(child) is to save taxes. Navios Maritime Midstream is tax-exempt. Bring the number of ships they have from 4 to 11; what does the dividend rate looks like then? 22.7% at IPO’s price.

The Bad

Ready to throw in the “hidden gem - I’m buying tomorrow at opening!” towel? Just a few minutes: Navios also comes with some downsides.

1) An IPO that is beyond nightmarish

While nowhere as bad as Sky Solar’s IPO, Navios is having problems pricing its IPO. The demand for it is abysmal: nobody seemingly wants it. Keep in mind that:

- Oil is getting destroyed in the market and prices are in free fall. Don’t even broach the subject of oil producers - they are getting murdered.

- Transport, for some reason, is also getting murdered

- Midstream companies are swarming the market: Antero Midstream, Shell Midstream, Dominion Midstream, Cone Midstream, those all happened in the last month

It’s shocking Navios is doing so bad in a market that is clearly bullish. Just for those reasons, the stock might crash at opening. That’s right: stocks might fall not because the company is not doing well or not a great investment, but because of market timing and trends. Because of a lack of buyers. Illogical? Absolutely. IPOs are incredibly volatile and many large investors won’t even consider them before analysts come out with ratings, and ratings usually come after the expiration of a wait period of 30 days or more.

Based on that, should you buy on opening? Should you wait a few hours or days maybe for it to stabilize?

2) The US imports less and less oil, reducing the needs for cargo shipment of oil

Oil prices are not crashing for no reason: sure, they want to isolate Russia and all, but one of the main reason is that the US is actually importing less and less oil. Recently, it found a massive reserve of oil on its territories and it is exploiting more and more of its domestic oil for political, financial and logistical reasons. This in effect means the US needs to import less oil by sea and the US, well, is one of the biggest consumer of oil worldwide.

3) Risk of shipwreck

With only 4 ships in its fleet, it goes without saying that, shall one of them sink, the company will be in big trouble. Navios Maritime Midstream, of course, is far from stupid and well aware of that risk: it is insured and even reinsured.

We have obtained marine hull and machinery and war risk insurance, which includes the risk of actual or constructive total loss, for all of our vessels. The vessels will each be covered up to at least fair market value, with deductibles of $250,000.

Another big risk with oil tankers is to cause another Exxon-Valdez. However:

Our protection and indemnity insurance coverage for oil pollution is limited to $1.0 billion per event. […] Any claim in excess of $80.0 million is reinsured by the International Group under the General Excess of Loss Reinsurance Contract. This policy currently provides an additional $2.0 billion of coverage for non-oil pollution claims. Further to this, overspill protection has been placed by the International Group for claims up to $1.0 billion in excess of $2.08 billion, i.e. $3.08 billion in total. For passengers and crew claims the overall limit is $3.0 billion any one event any one vessel with a sub-limit of $2.0 billion for passengers.

Exxon-Valdez, a massive oil spill, ended up with a final cost of $1.5B-$2B for the company (including punitive damage). Therefore, I do believe this insurance to be adequate and sufficient. However, even given all that, if there is a shipwreck or even a ship that is damaged badly enough to be inoperable or unsafe, severe disruption would follow and stocks would plummet, if only because of the uncertainty about possible lawsuits and insurance payments procedures. It goes without saying that, in case of a ship sinking or being put out of use, the dividend would be cut significantly (its chartering partners have a right to step out if a ship is unusable for a certain period of time).

With four ships, keep your fingers crossed. Sure, it’s unlikely and, again, there is insurance, but the risk is there.

4) 100% dependent on the demand for oil, which is currently in a downtrend

… but not for too long.

Navios explains this risk clearly in its prospectus. Basically, spot prices of oil, that is, the price you pay to buy oil right now, are quite low.

We may deploy some of our VLCCs or future product and chemical tankers from time to time in the spot market. Although spot chartering is common in the product, chemical, tanker and VLCCs sectors, product, chemical tanker and VLCCs’ charter hire rates are highly volatile and may fluctuate significantly based upon demand for seaborne transportation of crude oil and oil products and chemicals, as well as tanker supply. The World oil demand is influenced by many factors, including international economic activity; geographic changes in oil production, processing, and consumption; oil price levels; inventory policies of the major oil and oil trading companies; and strategic inventory policies of countries such as the United States and China.

Spot market deployment basically means a one-trip rent instead of the payer renting the ship for a fixed period of time. It goes without saying that the spot price is going to be higher than the time chartering (it costs more per day to rent a car for a day than for 10 years).

It also goes without saying that the maritime shipping industry is highly competitive and that new ships are entering the market all the time. Therefore, shall the demand for oil fall, so will the chartering costs and Navios’ revenues.

5) Its parents are doing okay, but not much more

Navios Maritime Midstream is a spinoff of Navios Maritime Acquisition Corporation (NYSE:NNA), which is itself 43.1% owned by Navios Maritime Holdings (NYSE:NM). This kind of strange structure is commonplace amongst companies with big ships and designed for tax optimisation. Both NNA and NM are doing okay, no more; both companies crashed around 25% in the last year due to weak oil prices. In fact, both of them barely have a market capitalization of a billion dollars. This sounds very meager, especially if you consider an average VLCC tanker (Very Large Crude Carrier, for transport of oil over the ocean, basically) cost $100 to $120 millions. You’d expect a company managing 44 ships (Navios Maritime Acquisitions) and owning 11 of those VLCC tankers to be worth billions, but it’s barely worth $459M today. Are ship that bad of a decaying asset that they have a negative value? If really those 11 VLCC boats/ships are worth $100 millions, why is the company worth so little? The market seems to have a generally very bad perception of maritime shipping of oil in general. In fact, the mother company, Navios Maritime Holdings (NYSE:NM) is down 50% off its peak:

Why is it going so bad? What’s going on? Based on the picture above, you’d believe they are on the verge of bankruptcy!

6) Risks, risks everywhere!

This might be a reliable industry in practice, but in theory, admit there is enough to be scared. So much could go wrong.

There is just so much that can go wrong here. Rising fuel costs, bad exchange rates, ship held in a port somewhere, ship lost at sea, ship’s motor broken and crew stranded on the ocean, change in laws, new docking fees, new taxes from a country, pirates, an increase in maintenance cost… This does sound like a risky proposal. What if they lose a key client, for instance? What if one of their only two clients goes bankrupt? What if the ships get stolen? Okay, that musn’t happen too often, but still - this is a business that operates in dozens and dozens of countries, all with different customs and regulations. What if there’s a storm? Okay, okay, they have insurance - but by buying this company, you are 100% trusting the people who manage the company. But then again, you do that with almost every investment you do.

Conclusion

So, what is it? A safe-growing and onerous dividend that you can collect until the end of your days, or another company that will plummet 50% from its opening price? Have I really found something that Wall Street overlooked completely? There is a lot to like from Navios and I think it’s worth a bite. It’s perhaps not the most aggressive purchase in the history of IPOs, but I foresee the dividend as stable, growing and secure. To quote its prospectus for another company it launched in 2007, Navios Maritime Partners L.P. (NYSE:NMM):

We are an international owner and operator of drybulk carriers newly formed by Navios Maritime Holdings Inc. (NYSE: NM), a vertically integrated seaborne shipping company with over 50 years of operating history in the drybulk shipping industry. Our vessels are chartered out under long-term time

…then again, the IPO price of that company was 20, and the stock now lingers at $13.77. But then again-again, the dividend went from 17.5 cents in 2007 to 44.25 cents today. Had you held, you would have earned roughly a 25% return in 7 seven years. I’ve seen worse. Oh, and the company survived the financial crisis.

VERDICT: Am I a buyer at $20? Yes, I am. Hidden gem that flew under the radar. Risky for sure, but also a very attractive business model. I like the extremely solid dividend and while it might crash in the days and weeks that follow the IPO (by no more than $2-$3 because of the dividend), I am confident enough in the company. Buying 100 shares at $20 at opening tomorrow (hopefully grabbing them even a little bit cheaper due to lack of interest).

UPDATE 11/13: I’m not sure what happened (?). The stock opened out of the blue. The IPO price was $15, FAR below its expected range. This has been a nightmarish IPO from beginning to end (see: point 1) and with this super-low valuation, it goes without saying the company is even more attractive. In all cases, my order somehow randomly passed at $13.30 for 200 shares. Am I stuck with a company that won’t move for years? Probably, but I’m still happy about my purchase. Great attractive dividend and a far better price that I expected. I have never seen an IPO work like that before.

Any idea what went wrong with this? If oil price goes up, will this ticker pick up? Are you still holding the bag or did you get out?