Remember when I said there were several outstanding IPO in the pipeline? Well, yeah. Today’s evaluation will be Axalta Coating Systems which boasts its slogan “Built for performance.” As opposed to what? Built for failure?

All bad puns aside, what exactly is Axalta Coating Systems? Well, it’s a company that manufactures coating; basically, paint. I’ve never invested into a company that makes paint before. Yes, I do know coating and paint are different, but to me, if it’s colorful and used to cover something, it’s paint. End of the line. Let’s just agree that Axalta manufactures special paint. It creates paints that goes on cars, industrial stuff (valve, tubes, levers…) and even trains. But is it a good investment?

Contents

- 1 The Good

- 2 The Bad

- 2.1 1) $3.8billions in long-term debt

- 2.2 2) Mediocre growth

- 2.3 3) Not particularly cheap

- 2.4 4) In case of an economic downturn, Axalta will have trouble staying afloat. Let’s hope that doesn’t happen

- 2.5 5) Difficulty creating value for shareholders

- 2.6 6) Barely any competitive advantage.

- 2.7 Conclusion

- 2.8 Share this:

- 2.9 Related

The Good

1) Probably the safest industrial investment in the history of industrial investments

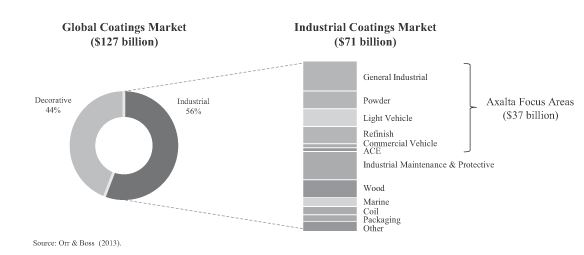

The company deals mostly with cars and truck coatings, but also provide coatings for “industrial machinery, electrical insulation, automotive components, architectural cladding and fittings, appliances, outdoor furniture and oil & gas pipelines.” Around 83% of their sales, however, comes from the cars, trucks and trains market, including repainting and the coating of equipment and pieces. This is not something that is going away. The market itself is massive, growing and here to stay:

In other words, Axalta is no Myspace or Twitter that is going to go out of style in 5 years. As long as we’ll need cars, we’ll need companies like Axalta. I don’t see any of the major 4 players (Axalta, PPG, Akzo and BASF) going out of business anytime soon. Axalta itself is a spinoff of Dupont and has been in business for over 150 years. It boasts an impressive number of employees (12,650) and does business in 130 countries. This is no small player: Axalta is a behemoth that knows precisely and entirely what it is doing. In my entire lifetime, I can count the number of massive companies that failed in a safe market on one hand.

One last thing: can Axalta eventually expand to another market, perhaps Industrial maintenance or wood? Other than by an acquisition, I don’t think so. I don’t think Axalta would earn much by spreading itself too thin in too many categories and I don’t believe the current sellers in those markets will simply let Axalta enter it without any opposition. I don’t think Axalta has much to win from a war in those markets.

2) Without a doubt a quality product with stable, reliable and diversified customers

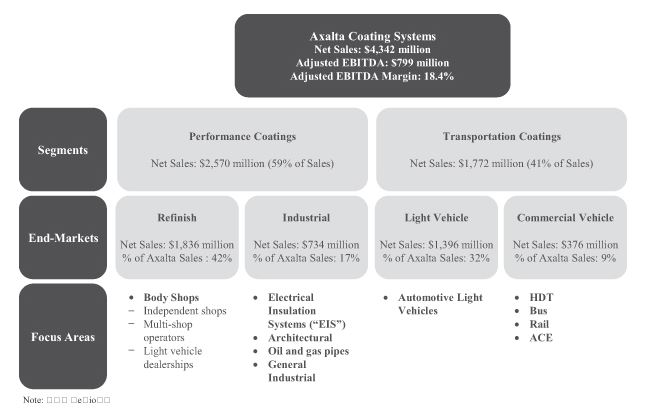

In addition to its vast experience and careful management (more on that later), Axalta has a diversified customer base that includes, for example, 80,000 auto body repair shops. In fact:

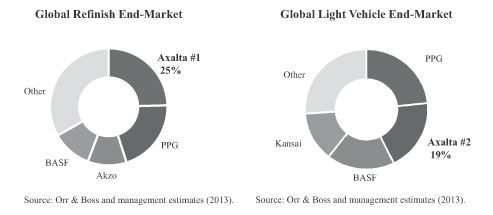

Somehow, it managed to take a simple idea (that is, coating) and become diversified. People will always need body shops and used car salesman will always need to have a few scratches covered before reselling a car for way too much. With a vast experience and a solid product (car painting is far more complex that I thought, to be frank!) it makes little doubt Axalta is one of the best in what it does. Furthermore, it has a dominating position in two of the four markets above:

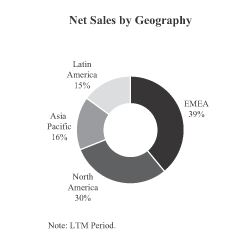

It also boasts a surprising diversification, really selling on the entire planet:

3) Oddly enough, it can grow.

I was quite surprised to find out just excited Axalta was about its car paint. It’s something we rarely think about, right? We choose a color when we buy a car and then we rarely ever rethink about it. But no, it released a full report on it. With the population growing, Axalta is in a market that is expected to be growing at 5-8% annually, worldwide. It makes sense: the more cars there are, the more business Axalta has.

4) It’s a play on China

… and, for once, there is nothing to copy. China is notorious for inviting a company to do business on its country, systematically copy its processes, patents and trade secrets, then kicking the company out of the country. Okay, I exaggerate a little, but China is well-known for being a realm of copying, where patents laws and protection do not apply. We all remember the fake Apple store that once popped up, with employees themselves being convinced they were working for Apple. In a country with an entire mall built around the concept of making fakes - fake expensive handbags, fake high-end watches, fake perfumes, fake trendy clothes and even fake sharpies, it should come as no surprise that the last time you want is to have all your stuff there for them to directly copy. Hell, an entire company is built around copying Apple. Anyway, I digress.

Axalta has absolutely nothing to copy. What, China needs to know how to make paint? There is nothing proprietary or unique to copy here. Someone who worked for Axalta for one week probably already knows how all their products are made. I suppose that if they really wanted to, China could copy them, but why? At best, they could perhaps equal Axalta’s product, but not expertise and distribution market. And a time where China’s equity market is opening on to the world, they have better thing to do than copy how some paint is made.

5) Extremely stable

Unless Axalta somehow messes up its accounting or becomes the victim of a major fraud, this company isn’t going anywhere anytime soon. I’d be very shocked to see it “totally missing profits expectation” at any time simply because it is totally unlikely. This is a predictable, slowly-growing, slowly-evolving market that is controlled by four major companies. This is quite similar to the soft drink market where pretty much nothing happened in the last 50 years: Coca-Cola, Pepsi, Snapple et al. are still in full control and we’d be shocked to see any of them disappear, or even announce significantly lower profits. If you told me Axalta still existed 50 years from now, I would have no trouble believing you.

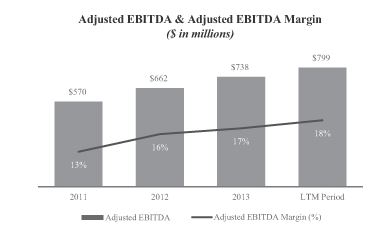

6) Great gross margin

The margin is probably the most attractive factor in its balance sheet: it’s surprising how much money they can make from painting a car (or selling paint to a shop). With an EBITDA margin (earnings before interest, that is money they pay on their debt, taxes, that is the tax on their profits, depreciation, that is their factory becoming older and amortization, that is, repaying their factory over a long period instead of paying it cash in one shot) at 18% and sales at $4.2 billion, we are looking at a very interesting business here. Think about it: this roughly means $799 millions in EBITDA per year, thus meaning the company is valued at roughtly 8-10 times that amount.

I’ve had my car repainted once after someone hit me. I can tell you: it’s not cheap. While the body shop itself might be making most of the money, I have no trouble believing high quality car paint is expensive as hell. And this is not a business that is going down neither: as long as people have car, they’ll damage them and want them repaired and repainted.

One last thing: its competitor, the only one publically listed, has known a phenomenal growth in terms of stock price:

The Bad

1) $3.8billions in long-term debt

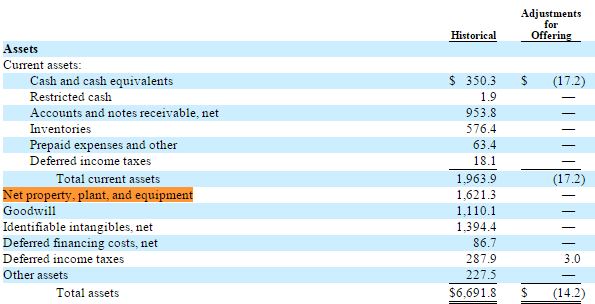

Huge interest charges every year. For a company with net income of $46 millions a year, this is huge. Sure, it owns valuable assets:

$4.1 billions in long-term assets

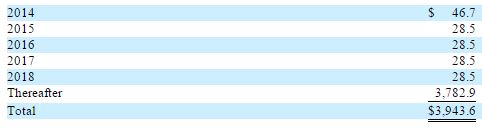

… but these assets remain long-term, uncashable assets. And they depreciate. In other words, if its debt became due today (which is obviously not the case at all), Axalta would be bankrupt. Let’s take a look at its debt:

It goes without saying the very vast part of its debt is renewable “after 2018.” When after 2018? Nobody but the great wizard knows. This is very significant and shall Axalta need other funds to renovate its building or cover depreciation, it might be in trouble and have to raise equity at a loss for current shareholds. Also, this makes Axalta vulnerable to interest rate (depending on the exact structure of its debt) and on its credit risk.

This, in my mind, is the number one risk that Axalta Coating Systems face at the moment: massive (but very far from overwhelming) debt.

2) Mediocre growth

Axalta does have room for growth, but not a giant bridge. As you probably guessed, coating isn’t the most exciting market in the world, nor is it the fastest growing. In fact, average growth in the preceding year stood at just 4% and future growth is expected to be at around that number. Even Apple faces a market is expected to grow at a minimum rate of 10% annually. And it’s not like Axalta can steal market share neither: it faces a fragmented market of several high-quality competitors

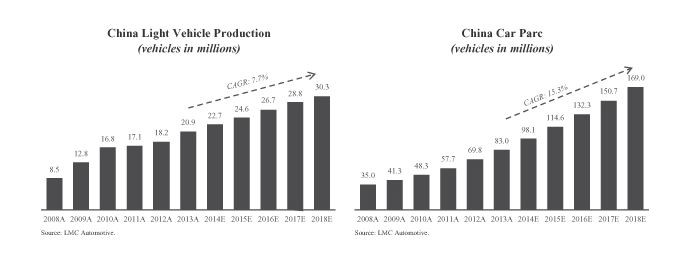

In fact, Axalta’s only real chance of any growth over 4% per year is China (remember that the worldwide expected growth is an average, and China’s number drive that average up; the rest will grow at a below-average rate). In fact, knowing that Axalta is a major selling of car coating:

The most generous sales growth estimates in the world

However, personally, I do not believe in Axalta’s chances in China.

First, the estimates above do sound a bit high to me, and if they actually materialize, what am I doing not investing into auto companies in China? In a county that is mostly poor and where the average salary is $4,755 (and that’s only for those who do work), I fail to see how most people could afford a $20,000 and up car, even on a monthly lease. And even if those estimates are correct, most of those vehicules are going to be used up and second hand vehicles imported from other countries (see: Cuba) on which Axalta will NOT make a revenue since cars only need to be painted once (and don’t tell me those people will have their cars repainted neither; they can’t afford it). This in effect means Axalta will not profit from this growth much. And even if sales of new cars explode, I do believe Axalta will not be the prime beneficiary of this growth because I believe the major part of the contract will go to local, chinese firms. Axalta is incorporated in the Bermudas and undeniably based in the United States (with a presence in Hong Kong, however).

3) Not particularly cheap

The current IPO range is $18-$21. I expect the average buyer (i.e.: you and me) to be able to buy it at $22-23. Before the IPO, Axalta has a market cap of $5.1B. At $22, we are adding roughly $990 millions in market cap. Adding in the premium for the IPO, you are looking at a business that is valued at close to $7 billions. Sure, I said above that it traded at 8-10 times its EBITDA, but when you do remove the I-T-D-A part, Axalta actually earns $46 millions a year, a 152 P/E ratio. Sure, P/E doesn’t tell everything, especially for IPOs, but remember the organic growth will average 4-6% and I fail to see exactly how Axalta could capture market share from its (presumed) competitors. Its margin seem to stabilize too and it would make sense that they continue around that amount, so an increase there is unlikely.

We are thus looking at a company that will grow at most 6% per year, which may or may not translate in direct profits (maybe other costs will rise). Under this view, the IPO is certainly not cheap.

4) In case of an economic downturn, Axalta will have trouble staying afloat. Let’s hope that doesn’t happen

Axalta is one of those companies that is very vulnerable to any downturn. Because of its relatively large debt and fixed assets, Axalta will not do too well during an economic downturn. Indeed, shall the amount of cars sold per year fall significantly, Axalta will endure heavy losses and will need, sooner than later, to raise more capital to be able to stay afloat. This will wipe out current shareholders value by 50% of more. In my mind, Axalta needs 4-5 of growth and/or stagnation to really be able to grow and stabilize, reduce its vulnerability to the market and be in a position to see longer term contracts that could provide a cushion during a downturn. Shall the economy falter in 2015 or 2016, expect to lose a lot.

While a great company, Axalta is simply not one of those companies that will reward shareholder handsomely. How could it do it? By buying back shares? Not so close to an IPO, no. Dividends? Axalta is barely profitable and I don’t foresee a dividend anytime soon (its own prospectus state dividends are far away). So how are you, as a long-term shareholder, supposed to make money? Entirely from the stock price rising. Except that Axalta is not one of those business that focuses around its share price. It’s not, for example, a Solar Sky that could announce a big new project that will triple its cash flow or a Freshpet that could announce a 40% growth in its sale. Axalta is a pure industrial play and will depend on too many factors, including the economy, sales of cars, new trends in the automobile industry, new process in coating, expiration of patents, leaking of trade secrets, new competitors entering the field (see: point 6, little barrier to entry) and so on to have a stable, reliable, growing stock pricce. Really: a 5% growth in profits will barely affect its stock price.

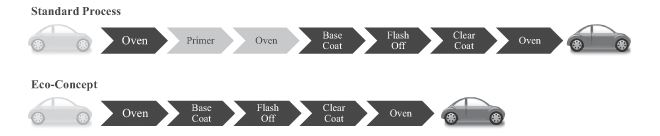

6) Barely any competitive advantage.

I have read Axalta’s prospectus and I fail to see what differentiates them from any other competitors. Look at this picture from its prospectus for example:

It saves two steps. Okay? But does this increases the cost of other phases? If not, how much do we save per car?

Axalta then pretends its process, which saves two steps, reduces costs. It goes as far as pretending new environmental norms are in favor of lighter car and that “its coating process reduces the overall weight of the car.”

I think that this is about as far as you can stretch an idea before it utterly silly. What’s next, its paint reflect more sun so the car runs cooler and it saves oil? Until I see hard data or until a car coating expert explains how efficient and genius Axalta Coating’s process is, I simply won’t believe it. This sounds like magical thinking at its best.

Still, it’s not all dark: keep in mind Axalta has an advantage since it’s such a big player. It’s one of the few players in the field able to take on a major contract from a major car manufacturer.

Conclusion

A solid company that will perform very well on its first year on the market, Axalta is a solid IPO that should seriously catch your attention. A light industrial play with a focus on the consumer market, Axalta is well-run, well-managed and very good at what it does. In fact, I’ll never make fun at it for making paint ever again, a process I discovered was far more complex than I originally thought. Axalta evolves in a competitive market and its growth opportunities, other than organic, will be minimal, but consistent. I believe it has a slight, but not considerable advantage over its competitors due to its innovative coating process and relationship with major customers, as well as its size (lower cost, abilities to take on big contracts, etc.). It is a stable, reliable, lucrative, well-managed and very competent company that will not face any significant downturn momentum other than a major economic crisis.

Verdict: Yes, absolutely, I would buy at a price of $22. Axalta is an easy and safe way to earn 8%-14% per year (4% organic CAGR (compounded annual growth rate) plus its net profit should average at 4-10% of its sales in a few years). When coverage is initiated (usually 30 days after IPO), analysts will have a “buy” rating on it, and the stock should go up. In my opinion, this is either a one-year play (which should earn you a 20-30% return from its opening price of $22) or a very long-term play (during which it will average a relatively stable 8% annual return). However, there are three excellent IPOs coming this Friday and I have little money left. I will put an order to buy 100 shares at $22 for the long-term. I will have to wait 6-8 months to buy more, at which point it will probably be too late (the stock will most likely be over $30 already).

UPDATE 11/12: Managed to grab some from its launch price, at 9:49am. Bought 100 shares @ $20.22, lower than the $22 I expected. Will rebuy if it goes around $19.50

No comments yet.