**Update 11/25: Rebuying as soon as the downtrend ends.

It’s at least worth taking a look. The Habit, a fast-growing burger joint based in the United States, is having its IPO this week, probably on Thursday, and it’s by far one of the most popular upcoming IPOs are the moment. In fact, it’s almost as hot as its grills.

So the question stands: should you take a bite of this IPO? Let’s analyze the good parts and the not so good part.

Author’s note: this is the report that has taken me the longest to write so far. 3 days of work, around 14 hours total.

Contents

The Good

1) Look at this little baby:

Tell me you wouldn’t absolutely devour that.

I’ll be honest, the main reason I want to invest in this company is because this burger looks delicious as hell. Look at the picture above and tell me you wouldn’t absolutely devour that. I think this is the most perfect picture of a hamburger I have ever seen in my entire life. Absolutely every single little thing looks perfect, from its perfectly thick roast bun to its delicious-looking onions dripping from the top along the melted cheese, and of course the two great patties who just look perfectly juicy.

Honestly, hats’ off to whoever took this incredible photo. As far as I’m concerned, this photo was worth every penny The Habit paid for it, and I have no idea how much this photo cost in the first place. Compare that to the best photos of Big Mac, Whopper and , the three best-selling hamburgers in America:

These look absolutely great, of course, but The Habit simply looks better.

Are those great pictures? Sure they are - they’re outstanding pictures in fact, but if you had to choose between those and the one above, honestly, which one would you pick? Which one on the list looks the best? Keep in mind all those companies have far more money than The Habit, so they can easily afford at least as good pictures as anyone else. In my humble opinion as a burger aficionado, only Wendy’s comes close, and then again not that close.

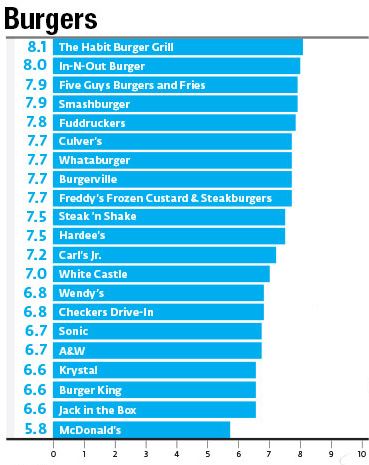

And The Habit’s burgers don’t just look good, they also taste good; in fact, they have just been voted the best burgers in America.

Source: Consumer Reports National Research Center.

The Habit scored at the top: it even beat Five Guys’ burgers, and believe me, Five Guys has excellent burgers. Of course, keep in mind there significant margin is 0.5, meaning that given how the study was made, The Habit is not necessarily better than, let’s say, Burgerville, and the different might be due to randomness and not a preference for its burgers per se. Still, isn’t it nice to stand at the top? Isn’t it nice to be recognized as the best burger from a fast-food in America?

On another note, McDonald’s, pull yourself together! 5.8? Wow!

2) Prime position in the market

The Habit has a prime spot in the market for one good reason: McDonald’s is getting ripped to pieces. Oh, don’t worry, it’s not going anywhere anytime soon, but the era of McDonald’s hegemony has definitely ended.

What happened is not clear. It’s quite a weird story, to be honest. How could a company be so dominant for so long, and then get completely beaten at its own game, which it supposedly mastered, by newcomers? Make no mistake: McDonald’s didn’t stand idle while its competitors rose to (wild) success. For instance, when Starbucks started to become really successful, McDonald’s hurriedly launched McCafé, which worked quite well, sure, but nearly near as well as Starbucks. Even today and despite McDonald’s best efforts, to claim that McCafé competes with Starbucks would be silly.

Also, when bigger, fresher and tastier burgers came into the picture, McDonald’s launched its “Angus burger,” trying to position itself as a premium burger joint, and failed miserably. One reason, in my opinion, was the contradicting message it sent: “Our new Angus burger are fresh, delicious, and made from 100% quality beef.” Okay… but what about the Big Mac? What kind of meat is in the Big Mac then? What have I been eating for so long?

Needless to say, McDonald’s massively failed to compete in the fresh, high-quality, healthy ingredients food industry. In the early 2,000 for instance, McDonald’s invested heavily into Chipotle, only to drop them at the worst possible moment (at its IPO in 2006). The reason it did that, I have no idea. McDonald’s claimed it wanted to focus on “core assets,” which is a cute way to tell investors, “we aren’t telling you the real reason.” In my opinion, McDonald’s simply thought Chipotle was not going to succeed long term and saw an easy exit door, along with a big cash out, at the eve of its IPO.

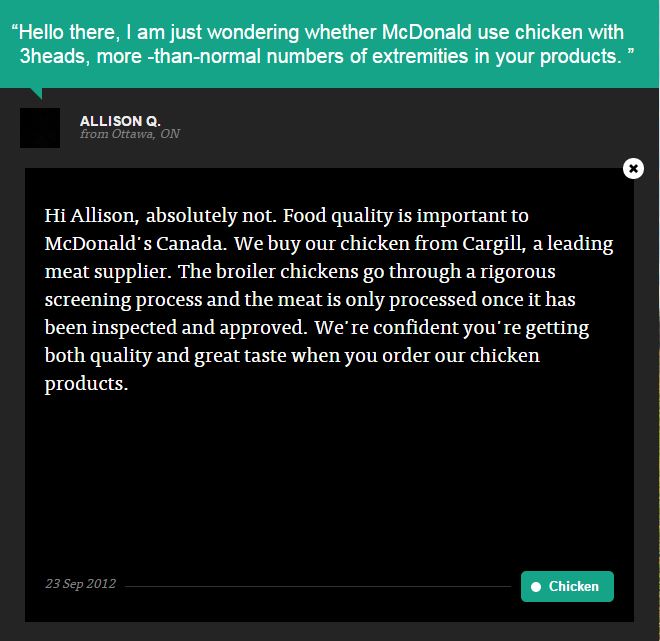

McDonald’s then launched the most incredibly stupid and nonsensical advertising campaign of all times, called “Our food, your question.” I remember walking around Montreal one day and seeing its ads plastered on the walls and think, “Wow, this is retarded.” Man, that advertising campaign sucked. Here’s an extract from it:

wut

This program is a gold mine for little gems of the kind and really shows just how bad McDonald’s image is in its customers’ mind. It’s also a good proof the majority of people who eat at McDonald’s are complete idiots. Can you imagine if Starbucks answered a question, “Do you use coffee beans that have been irradiated by a nuclear fallout?” I’m glad to hear chicken with three heads or extra extremities don’t get approve through the process however. I have a feeling “Allison Q.” does not have a firm grasp of basic biology.

There were a couple of things that put a serious dent into McDonald’s image, a dent McDonald’s in my opinion won’t ever totally recover from, and if you don’t believe me, keep in mind the “finger in Wendy’s chili” incident still has massive repercussions to this day. Oh, the incident was 100% fake and a fraud, but it doesn’t matter, and you’d be hard-pressed to find someone today whose won’t first associate the words “Wendy’s chili” to “finger.” Yes, images are that powerful, and the “chicken with three heads” is one of those: nothing can disgust someone faster than imagining he’s eating McNuggets that came from a chicken with three heads. Try it.

Then, there was the Supersize me documentary which, while inaccurate and borderline retarded/mass-media-panicky, tainted McDonald’s image forever. From this point onwards, customers could only associate McDonald’s products with “unhealthy, fattening, chemical, dangerous” even though this is, again, 100% false. And McDonald’s didn’t exactly help themselves by offering 5 cents supersize options neither; for a multinational worth several billions, it completely misread the market. Its “served in 60 seconds or it’s free” is another such blunder in the series: it gave the impression that McDonald’s food was cheap and quickly rushed together (the message here is, “take your meal and get out so your seat can be occupied by another customer!”). Honestly, if you can fully prepare an entire order in 60 seconds, how great can the food really be? If anything, it gave the impression McDonald’s rushed through your order and wanted you out ASAP.

There was much more to hurt McDonald’s, most of it false: that fake report about McDonald’s food never rotting, those disgusting videos of “how McNuggets are supposedly made…” There was that “McDonald’s put antiemetic products in its food” crap and those lies that people loved to spread. There was that “100% beef” scandal which, again, while completely false, didn’t fail to torment its customers. McDonald’s is failing (well, it is not failing, but it is being ripped to shreds) because people associate it to chemicals, fat and all other nasty things the media advertise. Is that image even remotely true? Again, absolutely not, but it doesn’t matter: McDonald’s story really teaches us that, in our world, facts don’t matter, but the way you present them do.

Overall, I think people grew tired of McDonald’s. The restaurant become a synonym for “trite,” “hawkneyed” and “timeworn.” The fact McDonald’s prices exploded did nothing to help neither: today, you can get a “real” burger from Five Guys at the same price as McDonald’s. And why would you bother with pre-frozen, rewarmed, tiny “beef” patties when you can have a real fresh hamburger with every topping you want? In a world where a big mac now sits at an average price of $4.80, who wouldn’t pay a little bit more (the burger in the picture above is just $3.95, so less than a Big Mac!) instead for a seemingly far better product?

Perhaps overall, once you grow to a certain size, you are bound to fall, or at least stop growing. It’s the law of diminishing returns, I suppose. The market has changed: customers today care about what they eat, whether it’s natural and fresh, whether it’s good for them and they care about the way animals are treated. Customers today have far more disposable income than they used to: back in the days of our grandfathers, eating at McDonald’s was a special occasion, something to celebrate, something you were waiting for. Today, McDonald’s is the lowest possible standard of fast-food and its food is seen as being filled with chemical and additives.

McDonald’s is not going anywhere, but its era of domination is near an end. Can it do anything to reverse the trend? Sure: it can play on its fast service, low prices and best in the world logistics (have you ever seen a McDonald’s that ran out of fries? A McDonald’s that ran out of anything, while we’re at it?) It can choose to continue with its bizarre actual strategy of heavily promoting high-priced burgers while trying to keep its value menu in a tiny invisible subsection. Overall, I think McDonald’s will be satisfied with its current 0-1% sales growth per year. Still, it’s not a stock I would recommend purchasing at today’s level and I don’t see the trend changing anytime soon. McDonald’s has become the Wal-Mart of fast-food: slow, tedious growth. Its sales won’t ever see a 10% rise again, and will often decline slightly.

There is definitely room for a new burger joint.

People are tired of microwaved burgers. People are tired of reheated patties. People today want something fresh and exciting. People today have money and people today want quality. End of the line. There definitely is a room for a mid-priced, high quality burger joint. Habit doesn’t reinvent burgers, but it enters the market in a prime position at a prime moment. There definitely is room for The Habit in a sector that is usually overcrowded and filled to the brim.

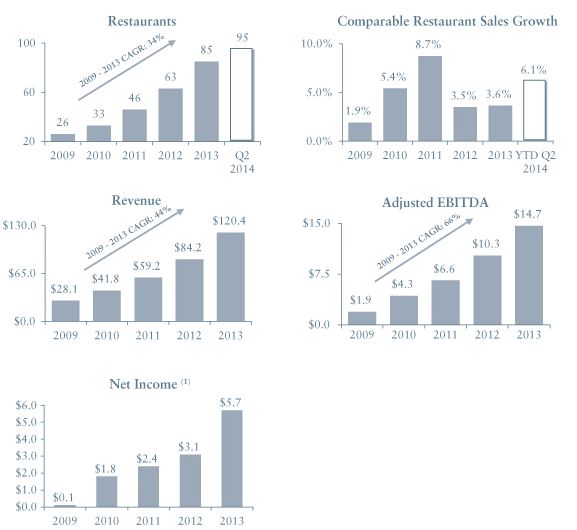

3) Insane growth

We can describe those graphs with one word: Wow.

It’s so good it almost looks suspicious (it’s not, however). You are pretty much looking at the picture of perfection here. Revenue has increased an average of 44% since 2009. Hell, every single metric of this company is on fire and if I woke up one morning to see that graph, I would start to believe I was dead and in heaven.

Let me try to explain with a comparison. Look at this pre-IPO metrics of a little-known company that you might have heard of, called Chipotle:

CHIPOTLE: Taken from Chipotle’s prospectus, before its IPO

And let’s look at how Chipotle fared since its IPO:

How Chipotle has fared since its IPO: 1,500% growth

Keep in mind Chipotle’s original IPO price was $22, and that it closed the day at $44. Let’s say you had bought at opening: you would be looking at close to 1,500% in gains.

See where I’m going here? The Habit has absolutely phenomenal numbers, much like The Chipotle had before its IPO. The Habit’s growth is simply extraordinary and shows absolutely no signs of slowing down. You are looking at at least 5 years of super-speed growth. An EBITDA growing at 66% per year? What? Oh, and the company is already well-profitable and has tremendous growth planned for its number of restaurants.

4) Terrific reviews

The Habit has extremely solid reviews, not only when it was voted “best burger in America,” but on very news and reviews website I could put my eyes on. Sure, you always have a raunchy guy somewhere who dislikes everything, but on most aggregate websites, The Habit is well-liked and is quickly established a loyal, dedicated and trendy (read: high middle class) customer base, which is only expected to grow over time.

According to customers, the line at The Habit can be as long as one hour as its most prominent locations during prime time. Yes, some people really wait one hour to be served, and its numbers tend to support that. This in effect means the restaurant can open more locations in the cities it already does business in, in locations it already knows well and where it’s already profitable.

There must be something about this restaurant, no?

5) Solid prospectus

A more comprehensive study of its prospectus is offered in “The Bad - point 4),” but rest assured I read its entire prospectus and barely managed to find anything negative or “not going superbly well” with this company. Let me give you an example. One common and easy way for restaurants to “cheat” in their report is to keep opening a ton of new, unprofitable restaurants to increase overall sales. In that way, even if sales at each restaurant fall, the total sales of the chain would increase because the chain would have more restaurants (imagine same store sales shrinking by 2%, but the total number of restaurants increasing by 5% - you would have an aggregate growth of 2.9% even though the chain is not doing well). A way to avoid this “cheat” is to look at “same store sales growth,” meaning that you look at how sales fare at restaurant already in place.

Well, The Habit answers this question::

Wow. Not even one negative quarter in 5 years. Not one single misstep in five years. Its prospectus reassures me that we have a company with a serious plan and the means to do it.

6) Hype!

This IPO is incredible hyped:`just by looking at everything that surrounds it, you’d think Apple is doing a second IPO. It’s very, very, very popular and a lot of people want in. I am not the only analyst of new IPOs, and many people and big firms have realized just everything I’ve been writing to you so far: that it’s very popular among customers and growing faster than my appetite for their burgers.

The hype is not going to die the moment this stock gets public: just because of the attention around this stock, you can expect a slow, steady growth in its stock price in the weeks and months that will follow the IPOs. And new restaurant openings will definitely support this rise.

The Bad

1) It’s just another place making burgers!

Chipotle had an edge that nobody else had: it was original, it was new and it responded to customers’ need for fresh, original, tasty food. It became a tremendous success because it brought something new to the market. But The Habit doesn’t have that. In fact, there is barely anything original about it. Here is what’s on its menu:

- Burgers

- Fries

- Salad

- Soda

- Milkshake

We’ve seen that countless times at a countless number of restaurants before. Try to imagine all the chains offering exactly that: Burger King, McDonald’s, Wendy’s, In-n-out burgers, Harveys, A&W, Five Guys, White Castle, Dairy Queen, Jack in the Box, Hardees, Whataburger… Do we really need another burger joint? What can “The Habit” offer that isn’t offered by the 100+ burger joints already on the market? And that’s just for fast-food that serves burgers, by the way: add-in the pizza fast-food, the chicken fast-food and all the others, and you have a very crowded market.

What does The Habit offers that is not being offered by any of its competitors? What’s the business proposition? Let me show what I mean to you:

- I say McDonald’s, you say… Big Mac

- I say Burger King, you say… Whopper

- I say Subway, you say… $5 footlong subs

- I say Stabucks, you say… venti latté

- I say KFC, you say… fried chicken and its secret recipe of 12,829 different spices.

- I say Olive Garden, you say… $9.99 unlimited pasta, bread and salad

- I say Chipotle, you say fresh burritos

- I say The Habit, you say… ???

Do you see where I’m going? It might be because it’s smaller and less known, but there is nothing in your mind that is particular to this one business. It’s just yet another burger joint. What specific product is offered there that competitors don’t offer? Chipotle offers fresh tortillas and prepares your meal in front of you. McDonald’s offer speed and low cost. Burger King advertises its bigger burger. Subway advertises low fat and made in front of you.

The Habit advertises charcoal-grilled burgers, called “Charburger,” quickly made in front of you with fresh ingredients. Well, that’s not bad. Are they going to create a trend around charcoal-grilled burgers? You know what, perhaps. Yeah, I suppose it could work. As a customer, I need to be told that I should go there because charcoal-toasted burgers taste better. Is that a marketing message that The Habit can relay? Perhaps, yes.

Overall, The Habit operates in an extremely competitive market with little room for mistakes. Do you know how many restaurants offer burgers? In addition to fast-food restaurants, I mean? Quite a few, yes. But The Habit does have a few things going for it: its low-price, fast service, great reviews and an original and novel proposition to customers.

2) Why an IPO so early?

Chipotle did its IPO at a time when it had over 500 restaurants. The Habit has 95. With that in mind, it’s clear The Habit is extremely eager to become public. But why?

Probably because it wants to expand quickly and add new restaurants. Without a major player supporting them like Chipotle had McDonald’s, and with dubious access to debt financing at best, it seems clear their best option to raise capital was to go public. Around two years too early, in my opinion.

There are over 160,000 fast-food restaurants in America. You are investing in a company that has 92 of those. There are probably hundreds of little “The Habit” in that 160,000 lot. Why should we trust that this one in particular is going to become successful? Why would people go to The Habit and not A&W, Five Guys Burgers and so on?

With the IPO, at the middle of its $14-16 pricing point, The Habit will raise $75M (before $1-2M in fees; yeah, expensive, I know). How many restaurant can they open with this money? Fifteen, twenty at most? Where’s the plan to build 500+ new restaurants? How are they going to get the money for that? More shares, right after the IPO? So, in other words, dilution for those who originally buy in the IPO? While not bad on a financial level (if shares are sold at market prices, they get exactly the cash they are worth, and there is technically no dilution), shareholders never like the idea of more shares being sold at an offer and, as a result, shares always tend to go down after a shares offering for some reason.

Indeed, it would seem that the franchising option, a totally different business model, would be the way to go. But while franchising means faster growth, lower risk and less management, it also means lower profits. People who decide to open a franchise expect, and certainly deserve, a return. The profits franchise holders get represents profits shareholder don’t get. Furthermore, franchising comes with a bundle of problems of its own, including a certain loss of control over the restaurant’s operation. Indeed, a franchised restaurants might be poorly managed and damage The Habit’s image. Lastly, keep in mind that, to attract franchisees, The Habit will need to grow a bit more to really become attractive and start opening hundreds and hundreds of restaurants nationally.

Speaking of which:

3) Its growth is impressive, sure…

… but it happened during one of the most successful upwards market of all times, that is, from 2009 to now. Even I could have run a successful restaurant during that time period. Okay, maybe not, but you get the idea: what would The Habit have done had there been a crash since then?

Not many people remember that Chipotle’s stock crashed 66% - more than the index - from its top in 2008 to the bottom in 2009. Yet even during the financial crisis, Chipotle managed to churn out an impressive growth:

| Year | Revenues | Net Income |

|---|---|---|

| 2007 | $1.05B | $70.6M |

| 2008 | $1.33B | $78.2M |

| 2009 | $1.52B | $126M |

How? How did Chipotle do so well while earnings worldwide were plummeting? And, most important, can The Habit do the same in the event of a financial crisis? Right now, The Habit is growing at 40%, but all of it happened during “good” and “excellent” years. What if we get a “bad” or “terrible” year?

That kind of stock is a one-batter: if it stops growing, it crashes. To the ground. The Habit needs to keep increasing its number of stores by 20-30% per year minimum: any little shock right now could plain and simple crash (but perhaps not kill) it.

Remember: The Habit looks absolutely great, but there are at least 20 other “The Habit” right now in the United States, all with great and similar metrics. Furthermore, there are at least a hundred coming on the market in the coming years. With so much pressure, The Habit cannot afford to even slow down a little or shareholders will drop it and move to another company. If The Habit announces a year of barely 20% growth (which is still incredible) in 2015, the stock will crash because huge expectations are built into the company already.

The Habit is vulnerable to a prolonged, multi-year economical downturn and, unlike Chipotle, will have trouble surviving it simply because they have far fewer restaurants and locations than Chipotle had at the time of its IPO

The company might survive, but not the shares, and they might never recover. Remember that the IPO, while cheap if you consider the phenomenal growth of the company, is still at a premium P/E ratio of 45 and by the time you get it, the ratio will be close to 60. Ouch!

Put it close to McDonald’s estimated P/E ratios for 2014 of 19.1, Burger King’s P/E 33.0 and Wendy’s 24.9 and you have a pretty strong P/E. Shall The Habit fall down to a more average P/E, let’s say a still generous 30, you’d now be facing a share worth under $10 a share, or $9.86 precisely, a major and very quick loss.

4) Its restaurants are focused in one region, and it’s going to be hard to grow out of it.

Penetrating California’s market (in which it has plenty of room left for growth) is one thing. But how do they plan to expand in all other states? What’s its strategy to open stores in other countries? Let’s look at its restaurants distribution right now:

Again, compare that to Chipotle’s geographical mix at the time of its IPO:

Chipotle Mexican Grill, Inc. (the Company), a Delaware corporation, develops and operates fast-casual, fresh Mexican food restaurants in 22 states throughout the United States

You don’t market and sell a burger in Florida the same way you market it in California. You don’t market a burger in Canada the same way you do it in the United States neither. What’s The Habit’s strategy for growing out of California? How do they plan to get themselves known in other states, first of all? The prospectus is relatively quiet on that - perhaps because The Habit could maintain its current growth rate in California alone.

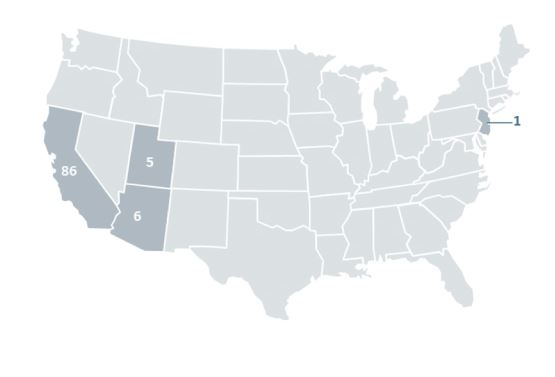

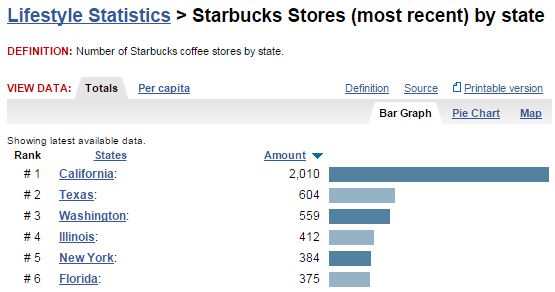

Selling stuff in California is pretty easy. Simply put the word “healthy” somewhere in your marketing, set your price at twice what your competitor charges and customers will flock to your door. Don’t believe me?

http://www.statemaster.com/graph/lif_sta_sto-lifestyle-starbucks-stores

And there is no trick there neither: California has 11.8% of the population of the United States, yet 24.4% of all Starbucks in the country. And its population concentration is quite high as well, it’s the 11th state with the highest population density so, technically, Starbucks would need to open fewer shops in California than in, let’s say, Colorado, to offer its products to the same percentage of the population.

So, can The Habit enjoy the same success in other states, perhaps even some were burgers are taken so seriously they are basically worshiped? Can it manage the logistics to deliver fresh burgers in ten, fifteen, twenty, forty different states, all with different customs, traditions, habits (!), taxes and regulations, while still maintaining its prime quality and affordable prices?

The only answer to that question can be obtained by taking a look at its management.

In other words, are the managers good enough to both achieve an ambitious national expansion program while still increasing sales and profits at its existing restaurants? Are they good enough to juggle with complex sales data in an often recondite market to not only maintain The Habit’s phenomenal growth and success, but expand it exponentially? Are they skilled enough to eventually manage a multi-billion company? Let’s take a look:

Russell W. Bendel was appointed Chief Executive Officer and President of The Habit Restaurants, LLC in June 2008 and was appointed Chief Executive Officer and President of The Habit Restaurants, Inc. in August 2014. Previously, Mr. Bendel was President and Chief Operating Officer of The Cheesecake Factory. Beginning in June 2001, Mr. Bendel worked at Mimi’s Café as Chief Executive Officer and President.

Good start, wouldn’t you say?

Russell W. Bendel was COO of The Cheesecake Factory (a fine dining restaurant) until close to or in June 2001. Here’s what happened during that period:

Cheesecake returns while under the command of The Habit’s current CEO

And it’s not like the company crashed after. In fact, the stock price rose by another 200%. Of course, all of this cannot be commended solely on the COO, but… it’s nice, no?

Ira Fils was appointed Chief Financial Officer and Secretary of The Habit Restaurants, LLC in August 2008 and was appointed Chief Financial Officer and Secretary of The Habit Restaurants, Inc. in August 2014. H Previously, Mr. Fils served as Chief Financial Officer of Mimi’s Café from 2005 to 2008, after joining the company as Vice President of Finance in 2003. From 1998 to 2003, he served in various financial capacities with increasing responsibility which led to him becoming Chief Financial Officer at Rubio’s Restaurants, Inc.

Decent, wouldn’t you say? Quite a successful career, no? Mimi’s Café is a slow-growth, successful private business and Rubio’s Restaurants, Inc., was taken private at $8.70 per share in 2010 (it was then trading at around $7.41 per share). Not the wildest success, but not too bad for a company that did its IPO on the eve of the dotcom bubble, and then went on to survive another massive crash. Again, not every fault within the company can be attributed to one man; still, it goes without saying that Ira Fils has experience in managing a restaurant chain.

Anthony Serritella, Chief Operative Officer of The Habit Restaurants, LLC. joined The Habit Restaurants, LLC in 1997 as Vice President of Operations and was later appointed Chief Operating Officer. Beginning in 1991, Mr. Serritella worked as the Vice President of Operations for McAthco Enterprises, one of the leading Sizzler franchises.

Peter Whitwell, Chief Quality Officer of The Habit Restaurants, LLC. joined The Habit Restaurants, LLC in 2005 as Vice President. From 2001 to 2004 he was the Senior Vice President of Baja Fresh Mexican Grill, transitioning from the position of Senior Vice President of Franchise Operations and Quality Assurance, a position he held beginning in 1999.

Those are two other moderately successful restaurant chains (Sizzler and Baja). Perhaps not the most experienced managers in the world, but decent enough, no? I mean, 23 years of experience for the COO and 15 for CQO. Remember that both companies they worked for did well.

The next person is supposed to find high quality real estate assets for The Habit to open new restaurants. Read his summarized description and tell me whether you’d trust him to do just that or not:

Russell Friend, Chief Development Office of The Habit Restaurants, LLC in December 2010 as Chief Development Officer. Prior to that, he served as the exclusive real estate development consultant to The Habit Restaurants, LLC from 2007 to 2010. From 2006 to 2007, he served as Senior Real Estate Partner of P.F. Chang’s China Bistro after joining the company as the Director of Real Estate of Pei Wei Asian Diner in 2003. Mr. Friend attended the University of Arizona and Menlo College.

Decent, wouldn’t you say? 4 years managing and buying locations for a fast-growing, trendy restaurant chain with close to a billion dollars in sales today. Finally, the Chief Marketing Officer, who is supposed to be the one in charge of all promotional materials related to the company. This person is supposed to manage the entire message the company is trying to convey to its current and prospective customers in all of its advertising efforts:

Matthew Hood, Chief Marketing Officer of The Habit Restaurants, LLC in July 2014 as Chief Marketing Officer. Prior to joining The Habit, Mr. Hood served as Chief Marketing Officer at BJ’s Restaurants Inc. from 2008 until 2014. Prior to joining BJ’s Restaurants, Mr. Hood served as the national brand consultant for Google, Inc. From 2002 to 2006, Mr. Hood served in several leadership roles for Carino’s Italian Restaurants, including Senior Vice President, Marketing and Brand Development.

Yep, I think he will do just great. National brand consultant for Google? Chief Marketing of BJ, a widely successful restaurant? Wow.

The word that comes to mind to describe The Habit’s management is this one: solid. The management team is solid, experienced and extremely competent. You aren’t facing a group of teenagers who decided to open a restaurant on a whim: you are facing an entire team of veteran managers who have a very strong interest in growing the chain into a very successful venture. You have a managing team that knows what they are doing and who will do all the work necessary for exactly that to happen.

So yes, I believe The Habit can succeed out of California.

5)”This is the next Chipotle! Buy buy buy!”

There is too much hype around this stock and it’s going to be next to impossible to grab some shares at a decent price.

Everyone wants this stock. It’s almost as hot as the charcoal brickets it uses and there is literally so much demand surrounding this stock that getting it under $20 is going to be extremely difficult (current’s range is around $14-16; you are paying a 33% premium over its midprice of $15!). Remember how Alibaba priced at $68 and opened at $92.70? I sure do. It’s worth repeating it, but it’s so completely unfair to individual shareholders. Just because the demand is that great, even bigger than Virgin Americas’, you might end up not being able to grab shares until very late. For instance, keep in mind Chipotle was priced at $22 and opened at $44 (!). And keep it mind you’ll be investing into a company with a P/E close to 60, and not some multi-national like Alibaba: a relatively medium-sized fast-food with $120.6 millions in sale last year. Yes, on its first trading price, you are likely to overpay. In fact, someone buying the stock at $16 the day before the IPO will be able to easily resell it the next day for $19, a 18.75% return in less than a day. Crazy.

Conclusion

While The Habit is probably not the next Chipotle (then again, you never know, but it isn’t as original, nor backed by big players like Chipotle was), it remains a quickly growing, profitable, well-managed and very interesting company. Its IPO is very interesting and a lot of “big fishes” are going to buy. Expect the final offering price to be $17-18, above its current range, and expect to pay a little over $20 to buy at opening (which I plan to do).

Verdict: The Habit is absolutely worth taking a bite and risk/return ratio is incredible. I do believe The Habit has a lasting advantage and while I don’t think it will reach Chipotle’s success, I believe in its management and its abilities to consistently grow over time. This is a company that will most likely maintain its amazing 40% annual growth for at least three years. I’m 100% sure to take a bite at under $20 a share, probably around 250 shares. Between $20 and $22, I will most likely buy, but probably won’t get a return on that for a few months. Over $22, I would buy a small position, probably 100 shares. At $24, I will sigh heavily, cursing the morons who reap all the benefits from any even remotely successful IPO.

Now, I gotta find a way to go to California to eat these burgers. Note to myself: don’t write a financial evaluation when you’re hungry.

UPDATE 11/20: The stock opened at $31, far above its opening price of $18 and far above what I expected. If you ever wondered where the maxim “the rich get richer” meant, you now know the answer. This is ridiculous. Nevertheless, I grabbed 100 shares at $33.41, far fewer than what I wanted. It’s doubtful I will have any meaningful return on my shares for at least 12 months. Feel free to wait this one and buy on a dip. Thanks again for the support, follow me on Twitter or Facebook for more analysis.

UPDATE 11/20 (2): Look at that little beauty!

$600 in one day. 20% return. Not bad. Almost as pretty as their hamburgers. The question now is, can I make enough money to pay for a trip to California to go taste their burgers?

For all those who e-mailed me: no, this is not the time to sell. There might be a pullback, but The Habit is a fantastic stock to own.

UPDATE 11/21: Just some clarification for someone who e-mailed me. No, McDonald’s is not “finished.” It’s not going anywhere and I said so in my article multiple times. However, its era of domination and 10% annual growth is definitely over, and I don’t see it restarting anytime soon. Is McDonald’s still a good investment? For the dividend and capital conservation, yes. For anything else, no.

Re: the photo. Note that the Big Mac et al don’t really look like their pictures when you order them. Invariably flatter, drier, less impesive. The Habit burger photo is not a feat of photography. I live in So Cal. I eat there. They look exactly like that. That is why they will succeed, the question on this one is stock price.

Great detailing and the hard work you have put in can obviously be seen. I am just a week old in the stock market and it is a great pleasure to read your articles and learn so much from them. I have placed a limit order at $16.4 for this stock. Not too many shares but just to get a hang of it. Hope you can buy some at a decent price too. Good Luck !

Thanks for the nice comments, I really appreciate!

The speech right now on the Street is about a $17-18 final pricing (before opening price), so you’d be super lucky to get it under $20.

Well it din’t make a difference because it was nowhere close to what everybody thought. Still looking to make an entry in this stock world !

You didn’t address the dilution risk. Aren’t all the LLC Units / class B shares exchangable for class A shares after the 180 day lockup period? There is 3x the number of class B shares compared to class A shares, so the risk seems very high. Basically, this would triple the PE ratio.

Hi Darkhound, thanks for the comment. I did study the structure they have and the only real thing that irked me was the greenshoe option (Apparently, it wasn’T enough for them to buy the stocks at half price, they have to get the option to buy even more at this half price), but this kind of thing is commonplace.

As for the shares you mention, this was indeed a very small IPO, but the triple P/E is not going to happen because the overall number of shares will remain the same. A risk is indeed dilution due to a future emission (the IPO was so small, barely 5M shares).

I was thinking the triple P/E would happen upon conversion. Although the overall number of shares remain the same, the Class B shares have no economic rights (they only have voting rights), so they shouldn’t be calculated in the current PE ratio. What is that now btw, something like 70?

But upon conversion to Class A shares, they would get economic rights, so they should be calculated into a diluted PE ratio, which would be 70*3 = 210 (crazy). Or am I missing something?! Thanks!

So yes, I checked my work and the PE ratio is indeed 200+. These guys agree: http://www.bidnessetc.com/29647-heres-why-habit-restaurants-habt-stock-has-surged-after-ipo/2/

Crazy! If I had guts, I’d short from here.

I’ll check tomorrow and reconfirm with you on that. I am unconvinced so far.

Update: I have investigated the situation and found that bidnessetc is wrong, and my analysis is correct.

From Habit’s prospectus:

>After this offering, there will be 8,244,488 shares of Class A common stock outstanding.

>Total Class A and Class B common stock to be outstanding immediately after completion of this offering 25,252,754 shares (or 26,002,754 shares if the underwriters exercise their option to purchase additional shares in full).

Keep in mind Class B can convert to Class A, but on a 1:1 ratio, so the total number of shares will not change. The convertion is mostly for people who hold Class B shares to be able to sell on open market.

Thus, currently, EPS is $0.332 annually, a P/E of a little over 100. At the price I indicated (22, low indeed), the P/E was indeed close to 60. Keep in mind this is a trailing EPS; also, keep i nmind the PEG is 2.50 (assuming 40% growth), which is nothing extraordinary. Lastly:

>If you purchase shares of our Class A common stock in this offering, you will incur immediate and substantial dilution in the pro forma book value of your stock, which would have been $8.59 per share as of September 30, 2014 based on an assumed initial public offering price of $15.00 per share

The book value is thus $6.41 per shares and The Habit is trading at roughtly 6 times its book value (pro forma) compared to McDonald’s 6.91.

Based on that, I stand by my analysis. I knew I would have never made such a rookie mistake 🙂

Thanks for bringing this up to me.