I received an interesting question today about volatility ETFs:

Hey Fs, love your website

I just read your article about shorting VXX and was wondering why not short TVIX instead. It’s a double etf, meaning the decay is twice as high (or is it?). Also if you look at a graph, it crashed 90%+ this year while VXX crashed 55%+

Maybe there’s something I don’t get. Love ya

This is a point that I discussed on my stream about a year ago and that I studied extensively. Back in the day, I was looking at shorting UVXY, another leveraged ETF that crashed 93% this year so far (VXX is down 66% and TVIX is down 94%

There are two major problems shorting TVIX:

1.Lower market cap

VXX has a market cap of $1.49B. TVIX’s market cap is $290M. while UVXY’s market capitalization is $740M. VXX is bigger, by far, which creates several for short sellers. For instance, in periods of heightened volatility, your shares might be called, meaning that the person you borrowed them from decides to sell them. This, in exchange, forces you to cover your position.

While such a scenario has never happened to me, there is no guarantee it will never happen in the future. With a lower market cap comes a higher risk of being “called,” especially if volality was to stay for a couple of days. While none of my shares have ever been called - the broker can find “more” shares to short - I have had periods where some of the produts I was shorting were listed as “unshortable.”

For this reason alone, I would stay out of low-cap products or products with low trading volume. You have a higher chance of being called, which sucks (see: short squeeze).

Example:

You short 1,000 shares of TVIX at $20. It jumps to $40. You are down $20,000.

You think “no worries, I’ll just keep shorting until it comes back down, which it must eventually, right? Look at the graph.”

TVIX jumps to $80. You are down $60,000. Your broker calls you and tells you that you have to cover because your shares are being called. You are forced to take a $60,000 loss.

2. Much, much, MUCH higher risk

The biggest problems with shorting double-leverage volatility ETF is that your run is that much higher. During the 2011 summer scare, VXX jumped from $1,300 to $3,600, a nearly 200% jump:

During the same period, TVIX and UVXY jumped 500%, more than twice the amount of VXX:

Keep in mind this was a relatively small scare; the S&P500 “barely” crashed from 1,350 or so to 1,130, for a 16% drop.

Now imagine what would happen during a meltdown such as the financial crisis.

Yeah.

Conclusion: Shorting Volatility ETFs

TVIX and UVXY are products that can be shorted and I can certainly see the appeal; after all, both products crash 95% per year. Overall, don’t fail to see the trap here and the fact that even a small drop could cause massive losses. Over the long term, I prefer to short VXX because it is less prone to massive jumps.

Then again, it could be argued that, with TVIX and UVXY, you are running a higher risk, but for a shorter period of time. After all, if you short the product 6 months, the product will have already crashed by 50%. Even if it doubles from there, you are just going to break even. And that’s the best way to sum up shorting leveraged volatility ETFs: a short period of very high risk.

If I were to short TVIX or UVXY, I would short very small amounts and I would definitely check it every day. A good strategy could be to short the same flat amount every week or so; short $1,000 every week no matter where it is. After all, UVXY and TVIX never had a 12-months period where they ended up positive. However, you would still be facing problems finding shares at periods of high volatility.

All in all, shorting VXX, a much more liquid and traded product, seems overall better.

Since we have time, let us address one final question:

Hey F.S.

If holding VXX is so stupid, then why are so many big funds holding it then? Are they just stupid

Yes.

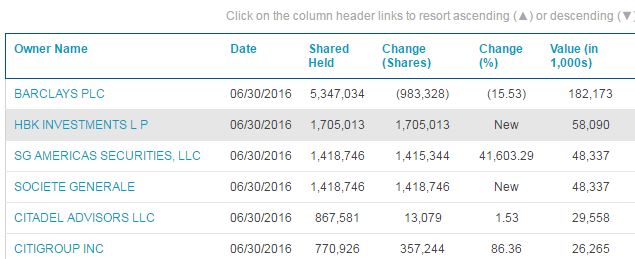

People assume that, just because a company is big, it’s good. People assume that, just because a company is known, these guys must know what they are doing. Look at the top institutional holders of VXX for instance:

People look at this chart and think, “Wow! Barclays! Citigroup! These guys must know what they are doing!”

They don’t. Now, make no mistake, a $40M position is nothing for these guys, but it’s still $40M that is being wasted. There is no reason to hold VXX, ever. You are literally owning a product that decays by 5% every month. These guys are throwing $2M in the trash every month.

If you want to protect your portfolio against a market crash, there are far better methods to achieve that result. You could diversify, of course, but you could also buy bonds, sells Out-of-the-money calls or even buy puts on your stocks. If you fear a market crash, you can buy puts on the S&P500 directly. And, ultimately, you can just play the volatility futures yourself. Which is something even a tyro knows how to do.

These volatility ETFs have no reason at all to exist, safe for the fact idiots keep buying them (and losing money with them). Even XIV, a reverse-volatility ETF, is dumb because you should really just short VXX instead.

So, are you short VXX?

Yes, I am. 1,000 shares.

FS,

I had a question on REITS.

Cominar has a 4.4% cost of funds on its mortgages

https://www.cominar.com/ENGLISH/Documents_PDF/Trimestriel_PDF/Trimestriel_Q216_EN.pdf Page 24. It has a Gross Book value of about 8 Billion in Assets with Debt to Gross book value of about 53%.

BTB Reit has a 3.86% cost of funds on its mortgages with less than 1/10th the market cap and Debt to Gross Book value of 67%.

http://www.btbreit.com/wp-content/uploads/2016/08/Q2-2016_EN_BR.pdf Page 36.

That makes very little sense. You would think Cominar’s costs of funds should be a lot lower but they are not.

Just wondering what you thought since you own them both.

Spent way too much time investigating this lol. Also fixed your comment which had the wrong link in it.

To sum it up:

COMINAR: At the end of the quarter, the

weighted average contractual rate was 4.40%, down 6 basis points from 4.46% as at December 31, 2015. As at June 30,

2016, the effective weighted average interest rate was 4.07%, compared to 4.05% as at December 31, 2015.

BTB.UN: As at June 30, 2016, the weighted average interest rate was 3.84%, compared to 4.08% for mortgage loans on

the books as at June 30, 2015, a drop of 24 basis points. As at June 30, 2016, all mortgages payable bear interest

at fixed rates or are coupled with an interest rate swap.

The interest rate has little to do with GBV and market cap. It has everything to do with the type of mortgage (variable, fixed, hybrid, etc.), when the mortgages where signed (a lot of BTB’s mortgages are very recent) and what type of properties is covered. Commercial, which CUF.UN owns a lot of, command a higher interest rate because the risk in holding them is higher.

For instance, I am worth perhaps 1/100,000th of Cominar, but I can get a mortgage at 2.25% at the bank tomorrow morning, far below BTB and CUF.

Hope that answers your question!

Thanks!

I suppose timing would be the biggest factor and so that means Cominar’s should continue to swing down for the foreseeable future. Making their 10% yield stick?

What do you mean by “commercial” properties? I always saw properties as Industrial, Retail, Office, Residential and Mixed. Commercial meant all excluding residential to me.

is the devastating market crash coming ? lol